The subscription economy has fundamentally transformed how businesses deliver value and how consumers access everything from entertainment to enterprise software. Yet beneath the convenience of recurring revenue models lies a labyrinth of sales tax complexity that catches many digital businesses off guard.

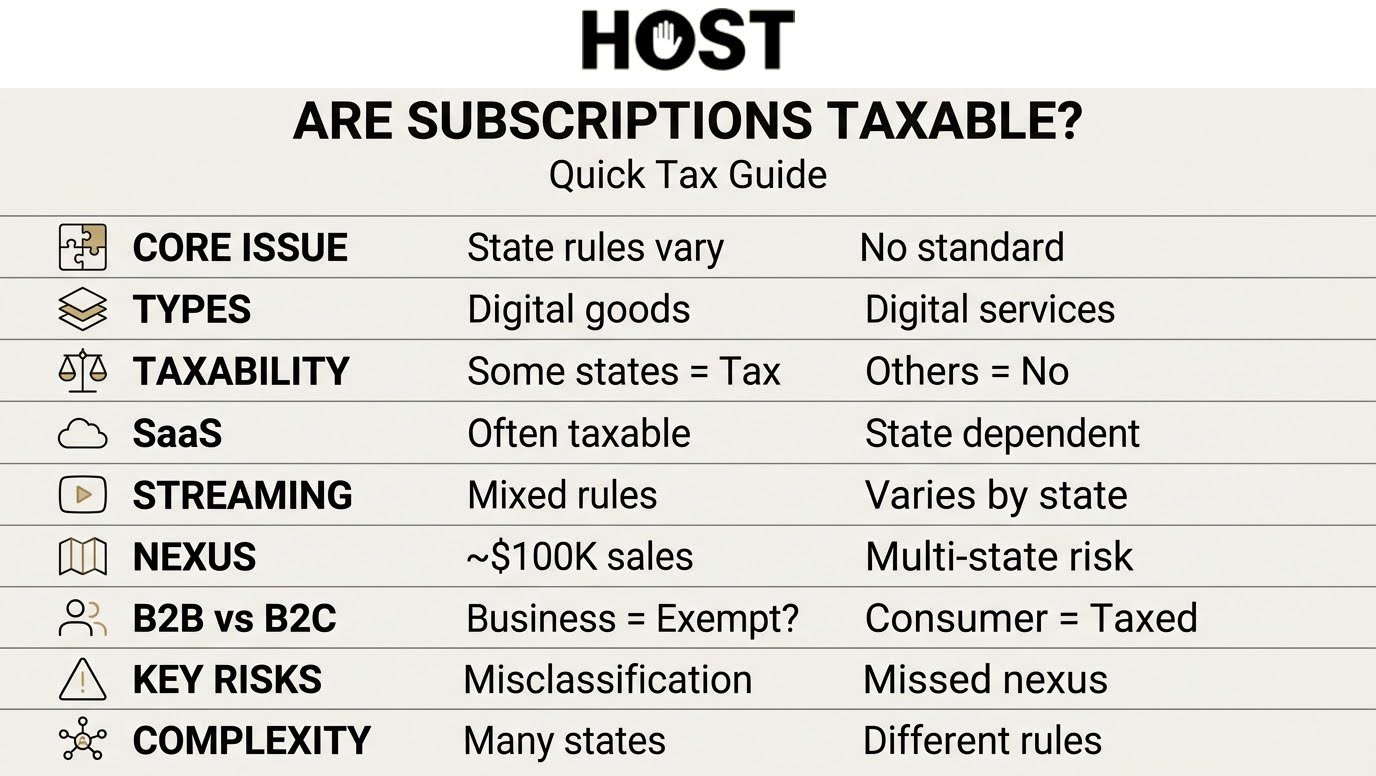

Subscription services exist in a gray area where state definitions vary wildly, what one state counts as a taxable “digital good” in another may be considered a non-taxable “service” in California.

The 2018 South Dakota v. Wayfair decision only intensified this challenge, expanding economic nexus obligations that now require subscription businesses to navigate compliance requirements across dozens of states simultaneously. If you’re uncertain about your current subscription tax obligations across multiple states, consider exploring a personalized sales tax consultation to identify potential nexus exposure and develop a proactive compliance strategy.

¹ Classification reflects general state tax posture, not guaranteed taxability. Actual tax treatment depends on product functionality, delivery method, customer type (B2B vs. B2C), and use case.

Understanding Subscription Service Taxation Fundamentals

The core challenge in subscription service taxation stems from how states classify what you’re actually selling. Most sales tax systems were designed decades ago for tangible personal property—physical goods you could touch, hold, and ship. The foundational question was straightforward: “Can you touch it?” If yes, it was taxable.

Digital subscriptions don’t fit these legacy frameworks. You can’t physically hold a Netflix subscription or ship a Salesforce license in a box. When information became digital and weightless, the old categories stopped working, forcing states to adopt wildly inconsistent approaches.

So states improvised, each inventing their own taxonomy:

Three Categories States Use (That Barely Contain Reality):

- Digital goods – Downloadable content like e-books or music files you “own”

- Digital services – Streaming or cloud access without ownership (Netflix, Spotify)

- Software-as-a-Service (SaaS) – Functional software accessed via internet (CRM, accounting platforms)

These distinctions tend to blur with the complexity of different subscription types. Your project management subscription counts as taxable software in Texas but slides through as a non-taxable professional service in Florida. Same product, same revenue model, completely different tax treatment depending on which bureaucrat is interpreting which statute.

The Tangible Property Debate

States approached the digital revolution in opposite directions. Some expanded their definitions of “tangible personal property” until the phrase included things that existed only as electrons dancing through fiber optic cables.

South Carolina decided cloud software qualified as “communications services,” a logical leap that would make a philosophy professor wince. Others maintained narrow interpretations, letting most digital transactions escape taxation entirely.

Economic Nexus: The Wayfair Trap

Here’s where subscription businesses face particular danger. You’re generating recurring revenue across state lines, and those economic nexus thresholds—typically $100,000 in sales or 200 transactions annually—arrive faster than you expect.

Launch with 100 subscribers at $50/month. Six months later you’re at 500. A year in, you’ve crossed nexus thresholds in a dozen states you’ve never set foot in. Somewhere around month eight, compliance obligations started accumulating like unpaid parking tickets, and you probably didn’t notice until the notices arrived.

The economic nexus thresholds by state are slightly different in every state, most hovering around $100,000, some counting transactions, some not.

B2B vs. B2C: The Same Product, Different Tax

Some states exempt subscriptions purchased by businesses for commercial use while taxing the identical service sold to individual consumers.

Real-world example: A cloud-based accounting software subscription priced at $50/month faces different tax treatment based on the buyer. In Louisiana, if you sell this subscription to an individual for personal financial management, you charge sales tax (around 9-10% with local rates). That identical subscription sold to a CPA firm using it to provide bookkeeping services to clients might qualify as a purchase for resale—making it completely exempt from sales tax.

Same software. Same features. Same price. Different tax treatment based entirely on who’s buying it and how they’ll use it.

States That Don’t Tax Most Subscriptions

Not every state jumped on the digital taxation bandwagon. Some maintained their traditional frameworks, treating digital subscriptions as services rather than taxable goods.

The Service vs. Property Framework

States like California, Florida, and Massachusetts (for most consumer subscriptions) generally don’t tax digital subscription services. Their tax codes focus on tangible personal property and specifically enumerated services, and digital subscriptions often fall outside these categories.

California maintains one of the more taxpayer-friendly positions. Unless your subscription involves tangible personal property or falls into specific taxable service categories, it’s generally not subject to sales tax. A SaaS platform, streaming service, or digital content subscription to a California customer typically doesn’t trigger tax obligations.

Florida exempts most information services and digital subscriptions under its current framework. The state taxes tangible personal property and specifically enumerated services, but most software subscriptions and digital content services don’t fall into Florida’s taxable categories.

States to Monitor for Legislative Changes

Just because a state doesn’t currently tax subscriptions doesn’t mean it won’t tomorrow. Several states actively debate digital service taxation including California, Florida, Massachusetts, and Missouri. The trend nationally moves toward taxation, not away from it. States see billions in potential revenue flowing through digital subscription services, and budget pressures make that revenue increasingly attractive.

Industry-Specific Subscription Tax Scenarios

Different subscription business models face different tax treatment, even within the same state. Understanding how states categorize your specific type of subscription helps predict your obligations.

Software-as-a-Service (SaaS)

SaaS represents the most commonly taxed subscription category. States that tax digital products almost always include SaaS in their frameworks.

Business Tools and Platforms:

- CRM systems (Salesforce, HubSpot) – Taxable in most comprehensive taxation states

- Project management (Asana, Monday.com) – Typically classified as taxable software

- Accounting platforms (QuickBooks Online) – Usually taxable as software or data processing

- Communication tools (Slack, Zoom) – Mixed treatment; some states exempt pure communication

The taxability often hinges on whether the state views your SaaS as providing software functionality (usually taxable) versus facilitating human-to-human services (often exempt). A video conferencing subscription might be taxable in Washington as a digital automated service but exempt in Florida as a communications service.

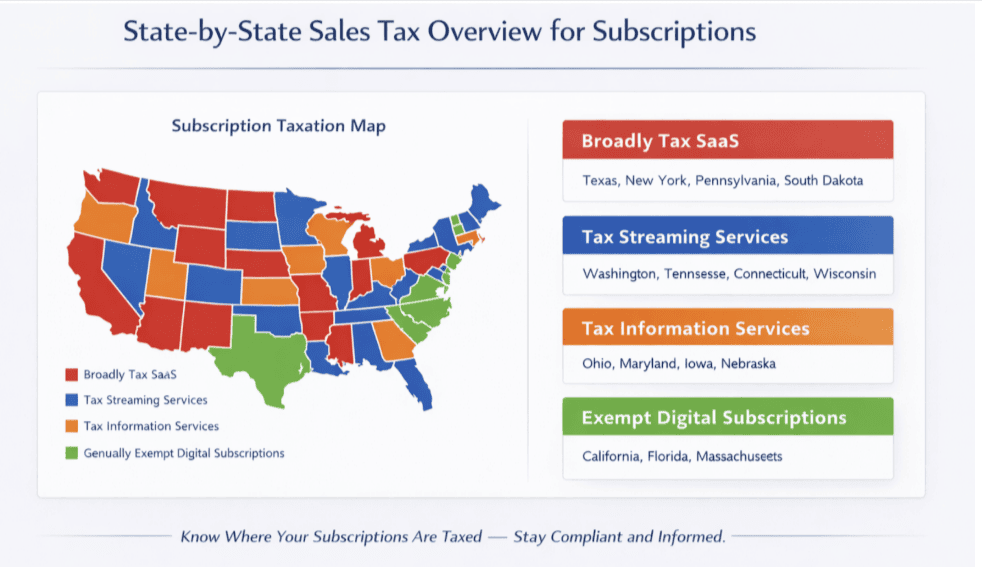

Multi-state complexity: A SaaS company offering project management tools faces taxability in Washington, Pennsylvania, Texas, South Carolina, and Tennessee while remaining exempt in California, Florida, and most other states. This creates pricing challenges—do you charge the same price everywhere and absorb tax costs, or pass taxes through to customers and risk appearing more expensive in taxing jurisdictions?

Streaming Services

Video and audio streaming services face inconsistent treatment that reflects ongoing debates about whether streaming constitutes a taxable digital good or an exempt entertainment service.

Video and Music Streaming:

- Netflix-style services – Taxable in Connecticut, Tennessee, Washington; exempt in California, Florida

- Spotify-model subscriptions – Similar treatment to video streaming in most states

- Educational video platforms – May qualify for educational exemptions if properly structured

Tennessee explicitly lists “digital audio-visual works” as taxable, capturing streaming services clearly. New York often exempts pure entertainment streaming while taxing business software—the same subscription model treated opposite ways based on content type.

Digital Media Subscriptions

News publications, magazines, and educational content occupy another gray area where states apply inconsistent logic.

News and Educational Content:

- Digital newspapers and magazines – Some states exempt as informational services; others tax as digital goods

- Professional research databases – Often taxable as information services in states like Texas

- E-learning course subscriptions – May qualify for educational exemptions if sold to schools; usually taxable to individuals

- Academic journals – Often exempt when sold to educational institutions; taxable to individuals

The distinction between selling to institutions versus individuals creates operational complexity. The same digital magazine subscription might be exempt when sold to a university library but taxable when sold to an individual subscriber.

Membership-Based Digital Services

Membership platforms that combine content, community, and tools face particularly murky classification challenges.

Common Membership Types:

- Online workout and wellness subscriptions – Usually treated as digital services (taxable in comprehensive states)

- Professional networking services (LinkedIn Premium) – Mixed treatment; information service versus software functionality

- Design software subscriptions (Canva, Adobe Creative Cloud) – Almost universally taxable as software

- Creative tools platforms – Taxable as software in most comprehensive taxation states

The key question states ask: What’s the primary value? If it’s software functionality, expect taxation. If it’s human-created content or human-facilitated services, you might escape tax in many jurisdictions.

For deeper guidance on whether your specific products are taxable, the product taxability guide walks through the analysis framework states use.

Common Compliance Challenges for Subscription Businesses

Subscription businesses face compliance challenges that one-time product sales don’t encounter. The recurring nature of your revenue creates operational headaches that scale with growth.

Multi-Jurisdictional Nexus with Recurring Revenue

Your subscription model amplifies nexus risk. You’re generating consistent monthly or annual revenue from the same customers repeatedly, which means you cross economic nexus thresholds faster than traditional e-commerce. A customer who subscribes in January contributes to your nexus calculation every single month. Scale that across thousands of customers, and you’re crossing $100,000 thresholds in states you barely thought about.

Customer Location Tracking Requirements

Determining where your customer is located sounds simple until you actually try to do it. States have specific sourcing rules—billing address, IP address, credit card billing location, or customer’s stated primary use location. For subscriptions, you need to determine location at signup and potentially monitor for changes. A customer who subscribes while living in California but moves to Texas mid-subscription creates a taxability change you need to detect and handle.

Changing Tax Rates Mid-Subscription Cycle

Tax rates change. Jurisdictions adjust rates, add local taxes, or implement new digital service taxes. Annual subscriptions create particular complexity—if you charge $1,200 upfront for a year of service and the tax rate increases six months in, how do you handle it? Most billing systems aren’t designed for mid-term tax adjustments.

Bundled Services Taxability

Many subscriptions bundle multiple elements—software features, content access, customer support, training. When different elements face different tax treatment, how do you allocate revenue? A SaaS platform including software functionality (often taxable), human customer support (often exempt), and training webinars (potentially exempt) requires “reasonable” allocation methods that vary by jurisdiction and auditor.

Exemption Certificate Management for B2B Subscriptions

If you sell to business customers who claim exemptions, you need to collect valid exemption certificates, verify they’re complete and current, maintain them for 3-7 years, and monitor expirations. For a subscription business with thousands of B2B customers across dozens of states, this becomes a significant administrative burden.

Audit Exposure from Misclassification

The biggest risk isn’t intentional tax evasion—it’s good-faith misclassification. You believed your service was exempt based on your reading of the statute. The state auditor disagrees. Now you owe back taxes for 3-4 years, interest, and potentially penalties.

Subscription businesses face particular audit risk because once an auditor identifies misclassification, the recurring revenue means substantial back taxes. One misclassified product category generating $50,000/month in a state with 8% tax means $4,000/month in unpaid taxes—$144,000 over three years before interest and penalties.

Common misclassification patterns:

- Treating all SaaS as exempt “professional services”

- Assuming digital content is universally non-taxable

- Failing to track when new states enacted digital service taxes

- Misunderstanding B2B exemption requirements

The top 10 e-commerce sales tax mistakes covers the errors that most commonly trigger audits and penalties.

Take Control of Your Tax Obligations

Subscription businesses operate in a fractured compliance landscape where the same service faces different rules for taxation in different states.

The businesses that thrive aren’t necessarily those with the best products or fastest growth. They’re the ones that built compliance into their foundation before it became a crisis.

Consider exploring a complete sales tax outsourcing approach. HOST has specialized exclusively in e-commerce sales tax for over 25 years, managing everything from nexus analysis to monthly filings across all taxing jurisdictions. For subscription businesses, this means proper classification of your services, monitoring economic nexus thresholds as you scale, handling registrations before you trigger obligations, and managing ongoing compliance without operational distraction.

Schedule a consultation to discuss your subscription service tax situation. We’ll analyze your current nexus exposure, identify potential misclassification risks, and outline what comprehensive compliance actually requires for your business model.

Frequently Asked Questions

If I’m a small SaaS company doing under $500K annually, do I really need to worry about sales tax on subscriptions?

Yes, and potentially more than larger companies with established compliance infrastructure. Economic nexus thresholds aren’t based on your total revenue—they’re based on your sales into each specific state. Many states set their thresholds at $100,000 in sales or 200 transactions annually per state.

The audit risk compounds for smaller companies because you typically lack the documentation, systems, and processes that larger companies maintain. When an auditor questions your classification of services or your exemption certificate practices, you may not have the paper trail to defend your positions. Early-stage compliance is almost always cheaper than retroactive fixes after an audit notice arrives.

How do I determine if my specific subscription service is taxable when states use different definitions for software, digital goods, and digital services?

Start by analyzing what your subscription primarily delivers: software functionality, digital content, or human services. States typically tax software functionality and digital content while exempting pure human services, but the boundaries blur significantly.

Ask these diagnostic questions: Could your service operate without human intervention after setup? If yes, states like Washington will likely classify it as “digital automated services.” Does your customer access prewritten software via the internet? If yes, states like Pennsylvania will likely tax it as electronically delivered software. Is the primary value information or data processing? If yes, states like Texas may tax it as information or data processing services.

For hybrid subscriptions that combine multiple elements—say, software tools plus human consulting—you’ll need to determine the “primary purpose” or potentially allocate revenue between taxable and exempt components. The nexus analysis service can evaluate your specific subscription model against each state’s definitions, providing clarity on where you face obligations versus where you’re legitimately exempt. Don’t rely on generic advice or what competitors say they’re doing—state auditors evaluate each business individually based on precise operational details.

I’ve been operating for two years without collecting sales tax on my subscriptions. What happens if I start collecting now?

Starting to collect sales tax now is the right decision, but how you handle past non-compliance matters significantly. Simply beginning to collect without addressing the prior period creates a documented trail that auditors can follow—your current compliance essentially proves you should have been collecting previously.

You have several options: File back returns and pay the tax you should have collected, absorbing the cost as a business expense (cleanest but most expensive). Pursue a Voluntary Disclosure Agreement in states where you have significant exposure—VDAs typically limit your lookback period to 3-4 years instead of 7-10 years, often waive penalties, and sometimes reduce interest. Or go forward only and hope you’re not selected for audit (the riskiest approach).

The worst scenario is doing nothing and getting audited. States can assess back taxes for the full statutory period (often 7-10 years), add failure-to-file and failure-to-pay penalties (sometimes 25-50% of tax due), and charge interest that compounds over the entire period. A $200,000 back tax assessment can easily become $350,000 with penalties and interest.

For subscription businesses, the recurring revenue nature means past non-compliance accumulates rapidly. Even one year of missed collections across multiple states can represent substantial liability. Address it proactively through VDAs before an audit notice arrives—you’ll have more leverage and better outcomes.

My billing system has tax calculation built in. Isn’t that sufficient for subscription tax compliance?

Automated tax calculation solves one piece of a much larger compliance puzzle, but it’s not comprehensive. Yes, these systems can calculate the correct tax rate based on customer location—but they can’t tell you whether your specific service is taxable in the first place, they don’t determine when you’ve crossed nexus thresholds, they don’t register you with states, and they don’t file your returns.

Think of it this way: your billing system might correctly calculate 6.5% tax on a Pennsylvania transaction, but if Pennsylvania doesn’t actually consider your subscription taxable, you’ve just over-collected from your customer. Conversely, if your system defaults to not charging tax because you haven’t configured it properly, you’re accumulating liability.

The critical gaps automation doesn’t fill include classification analysis (determining if your service is taxable under each state’s unique definitions), nexus monitoring (tracking when your sales trigger obligations in new states), registration processes, return preparation and filing, exemption certificate management, and rate change management when jurisdictions update their rules.

Automated calculation is valuable, but it works best when paired with expertise that handles classification, nexus analysis, registration, and filing. The sales tax calculation API combined with comprehensive management services provides both the technology and the human judgment layer that subscription businesses need.

We have both B2B and B2C customers. How do we handle the different tax treatment and what documentation do we need?

B2B subscription sales create compliance complexity that scales poorly without proper systems. In states that allow exemptions for business purchases, you must collect valid exemption certificates before treating any sales as exempt. Making exempt sales without certificates means you’re personally liable for the uncollected tax if audited.

Required certificate elements vary by state but typically include purchaser’s name and address, type of business and reason for exemption, purchaser’s tax ID or exemption number, signature and date, and seller’s name (your company). Some states have specific forms you must use; others accept uniform certificates.

Operational challenges for subscriptions: You need to collect certificates before the first exempt charge, not after. For monthly subscriptions, you need valid certificates covering the entire subscription period. Certificates often expire (some states require renewal every 3-5 years), so you need systems to monitor expirations and request renewals before they lapse. If a certificate expires mid-subscription, technically that customer’s charges become taxable until they provide a new certificate.

Many subscription businesses struggle with partial exemptions—where a business customer uses your service partly for exempt purposes (resale, manufacturing) and partly for taxable purposes (internal operations). Some states require you to charge tax on the non-exempt portion, which means tracking use case and allocating charges.

Best practice: Implement certificate management at signup. Make certificate submission part of your onboarding flow for business customers requesting exempt treatment. Use automated tools that validate certificates against state databases where possible. Set renewal reminders 60 days before expiration. And maintain organized digital storage—auditors will request certificates going back 3-7 years, and missing documentation means you owe the tax plus penalties.

I’m planning to expand my subscription service internationally. Do other countries have similar sales tax complications?

International expansion brings a completely new layer of indirect tax complexity, though the underlying challenges mirror U.S. sales tax issues. Most countries use Value Added Tax (VAT) systems rather than sales tax, but the compliance burden for digital subscription services is equally complex—and in some ways more stringent.

The European Union requires digital service providers to register for VAT and charge the rate applicable to the customer’s country, not your business location. With 27 member states and VAT rates ranging from 17% to 27%, you’re managing even more rate variations than U.S. sales tax. The EU’s One-Stop Shop (OSS) system allows single registration for all member states, which simplifies administration compared to registering in each country separately, but you still need to track customer locations, apply correct rates, and file quarterly returns.

Post-Brexit, the United Kingdom operates its own VAT system separate from the EU. Digital services to UK consumers require UK VAT registration once you exceed £85,000 in UK sales at a 20% rate. Canada uses both federal GST/HST and provincial sales taxes, with digital services generally taxable and registration thresholds at C$30,000 in sales. Australia’s GST applies to digital services provided to Australian consumers with a registration threshold of A$75,000.

Key differences from U.S. compliance: Most countries use destination-based taxation (customer’s location) rather than origin-based, similar to U.S. economic nexus. Registration thresholds are often lower than U.S. state thresholds. VAT systems typically have more uniform rules within each country, though rates vary. Some countries have simplified registration schemes specifically for foreign digital service providers.

The reality: international VAT compliance, while complex, often has clearer rules than the U.S. state-by-state patchwork. However, you’re now managing compliance across multiple tax systems simultaneously, each with different registration processes, return frequencies, payment methods, and documentation requirements. Most subscription businesses expanding internationally need specialized international tax expertise in addition to their U.S. compliance infrastructure.