Sales tax questions don’t wait for convenient moments. They arrive when you’re launching in a new state, reviewing an unfamiliar notice, or realizing your software charged the wrong rate for three months straight.

The answers matter because getting compliance right protects cash flow, prevents penalties, and keeps operations running smoothly. From nexus thresholds to marketplace facilitator laws, here are the sales tax questions business owners ask most, and the answers that actually help.

Hands Off Sales Tax (HOST) specializes in removing sales tax complexity from your operations. We’ve been 100% focused on sales tax since 1999. That’s over 25 years helping businesses navigate multi-state compliance. Co-founded by Mike Espenshade, with parent company TaxMatrix serving North America’s largest companies, we bring enterprise expertise to businesses of all sizes.

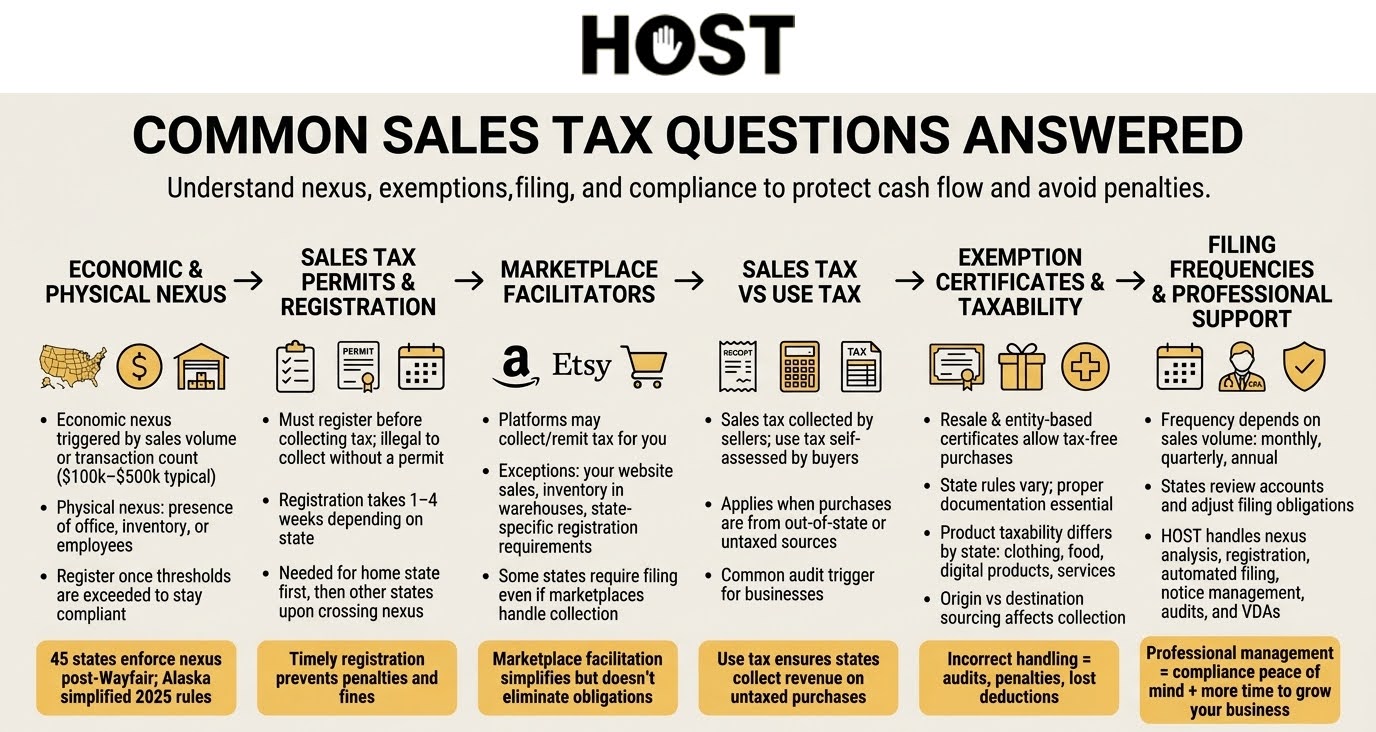

What Is Economic Nexus and When Do I Need to Collect Sales Tax?

Economic nexus creates a sales tax obligation based on your sales volume or transaction count—no physical presence required.

Following the 2018 South Dakota v. Wayfair Supreme Court decision, all 45 states with sales tax now enforce economic nexus laws. Each state sets its own thresholds, typically ranging from $100,000 to $500,000 in annual sales.

California requires $500,000. New York demands both $500,000 in sales and 100 transactions. Most states use $100,000.

Alaska recently simplified things. As of January 1, 2025, only the $100,000 sales threshold matters. The 200-transaction requirement disappeared.

Physical nexus still triggers obligations instantly. An office, warehouse, inventory, or employees in a state creates nexus regardless of sales volume.

You must register and collect once you exceed a state’s threshold. Monitoring your sales across jurisdictions prevents surprise obligations.

HOST provides comprehensive nexus analysis, reviewing your sales footprint to identify exactly where obligations exist. We handle registrations in required states while avoiding unnecessary ones elsewhere.

When Should I Register for a Sales Tax Permit?

You must register for a sales tax permit before collecting tax from customers. It’s illegal to collect sales tax without a valid permit because some states view this as tax fraud.

Register immediately once you establish nexus in a state. For your home state, register before making your first sale. For other states, register as soon as you cross economic nexus thresholds or establish physical presence.

Registration typically takes 1-4 weeks depending on the state. Some states issue permits instantly online; others require paper applications. You’ll need your FEIN, business structure details, and banking information.

Don’t collect tax until your permit arrives. Once registered, states assign your filing frequency and due dates.

Do Marketplace Facilitators Handle Sales Tax for Me?

Marketplace facilitator laws require platforms like Amazon, eBay, and Etsy to collect and remit sales tax on behalf of third-party sellers.

This simplifies compliance. You don’t need to collect tax on marketplace sales where the platform collects for you. However, three critical exceptions exist:

You still have obligations if you:

- Sell through your own website in addition to marketplaces

- Store inventory in states (like Amazon FBA warehouses), creating physical nexus

- Operate in states requiring registration even when marketplaces collect

Some states require you to register for a permit and file zero returns even when marketplaces handle collection. Check each state’s specific requirements.

Marketplace facilitation simply shifts collection responsibility for those specific sales.

What’s the Difference Between Sales Tax and Use Tax?

Sales tax is collected by sellers at checkout and remitted to states. Use tax is paid by buyers when they purchase taxable items without paying sales tax, typically from out-of-state sellers.

Use tax prevents tax evasion and ensures states collect revenue on goods used within their borders.

Use tax is self-assessed by buyers and paid directly to states, usually when filing business returns. Sellers don’t collect it from customers.

Common use tax scenarios:

- Buying from an out-of-state seller who doesn’t charge your state’s tax

- Purchasing items in a no-sales-tax state and bringing them home

- Using inventory purchased tax-free for resale in your own operations

- Drop shipping arrangements where the supplier doesn’t collect tax

The use tax rate equals your jurisdiction’s sales tax rate. Six percent sales tax means six percent use tax on untaxed purchases.

For businesses, use tax is one of the most common audit triggers. Many companies fail to self-assess on purchases from vendors who didn’t collect, creating substantial liability during audits.

How Do Sales Tax Exemption Certificates Work?

Exemption certificates allow eligible businesses and organizations to purchase goods tax-free under specific conditions. Buyers provide certificates to sellers at checkout.

Resale certificates let businesses purchase items for resale without paying tax, since end consumers pay later.

Entity-based certificates go to specific organizations like nonprofits, government agencies, schools, churches, any that qualify for tax-exempt status.

Usage-based certificates exempt purchases based on use, such as manufacturing equipment or agricultural supplies.

Each state has its own rules and forms. Some accept the Streamlined Sales Tax Certificate across 24 member states. Others require state-specific paperwork.

Sellers must collect and validate certificates before exempting transactions. Proper documentation is critical. If you can’t produce a valid certificate during an audit, you may owe the uncollected tax plus penalties.

Expiration periods vary. Some states’ certificates never expire. Others expire after 1-4 years and require renewal.

What Products and Services Are Taxable?

Sales tax applies to most tangible personal property, but rules vary dramatically by state. Product classification determines whether you collect tax, and how much.

Most states tax physical goods and tangible personal property sold at retail. But specific categories create confusion:

Clothing: Some states exempt all clothing. Others tax clothing above certain price thresholds. Connecticut exempts clothing under $100 but taxes luxury items. Some states tax athletic wear but exempt regular clothing.

Food: 32 states exempt groceries, but prepared food faces taxation. That rotisserie chicken from the deli? Taxable. The raw chicken you cook yourself? Exempt in most states.

Candy: The 24 Streamlined Sales Tax states distinguish candy containing flour (tax-exempt in some states) from candy without flour (taxable). A Kit Kat bar with flour may be exempt while a Hershey’s bar without flour faces full tax.

Common exemptions include:

- Prescription medications (nearly all states)

- Manufacturing equipment in some states

- Agricultural supplies and equipment

Origin vs. Destination Sourcing: Where you collect tax depends on whether a state uses origin-based or destination-based sourcing. Most states use destination-based sourcing, so you collect tax based on where your customer receives the product. A few states use origin-based sourcing, so you collect based on where you ship from.

Services present particular complexity. States differ wildly on which services face taxation. Digital products create special challenges. SaaS taxability varies by state based on specific characteristics.

HOST’s consultation services provide clarity on tricky taxability questions. Our team stays current on state-by-state rules and can advise on product classifications, service taxability, and industry-specific requirements.

Why Do Filing Frequencies Differ Between States?

Filing frequency varies by state based on your sales volume or tax liability.

Most states use three frequencies:

Monthly for high-volume businesses. Texas requires monthly filing for $12,000+ annual tax liability.

Quarterly for medium-volume businesses. California requires quarterly filing for average monthly tax liability of $100-$1,417.

Annual for low-volume businesses. Maine requires annual filing for under $50 yearly tax liability.

States determine frequency based on average monthly tax liability or sales volume. Most initially assign monthly filing, then adjust based on actual activity.

Frequencies change. States review accounts periodically and send notices. Missing these notifications leads to missed filings, penalties, and interest.

HOST manages filing frequencies across all registered states. We monitor for changes, update filings accordingly, and ensure every return submits on time.

Ready to Take Sales Tax Off Your Plate?

Sales tax questions multiply as your business grows, but your time spent answering them doesn’t have to. Understanding nexus, exemptions, marketplace rules, and taxability is essential since managing compliance across dozens of states is another matter entirely.

Every hour spent researching rules, filing returns, or responding to notices is an hour not spent growing your business. Professional management eliminates guesswork and prevents costly mistakes.

What HOST Delivers:

- Nexus Analysis: Determine exactly where you’ve triggered obligations

- Sales Tax Registration: Handle registrations in all required states

- Automated Filing: File returns monthly, quarterly, or annually based on each state’s requirements

- Notice Management: Interpret and respond to confusing state correspondence

- Audit Defense: Organize documentation and defend your position during audits

- VDA Support: File voluntary disclosure agreements to limit back taxes and penalties

Whether you’re managing nexus in multiple states, dealing with marketplace sales, or simply overwhelmed by filing deadlines, HOST handles the complexity so you can focus on sales instead of tax.

Contact HOST today to discuss your sales tax needs or schedule a free consultation. Let us answer your sales tax questions and take compliance off your plate entirely.

Want to learn more? Download our free guide: “10 Sales Tax Mistakes E-Commerce Sellers Make.”

Frequently Asked Questions

What happens if I don’t collect sales tax where I have nexus?

You remain liable for uncollected tax, paid from your own funds. States can assess back taxes, penalties (often 10-25%), and interest. The longer non-compliance continues, the larger the liability grows.

Do I still need to collect sales tax if I only sell on Amazon?

If Amazon collects sales tax on your marketplace sales, you don’t collect again on those transactions. However, if you also sell through your own website or store inventory in FBA warehouses, you may have additional obligations in those states.

Can I use the same exemption certificate in multiple states?

The Streamlined Sales Tax Certificate works in 24 member states, but many states require their own specific forms. Always verify which certificate format each state accepts.

How do I know if my products are taxable in a specific state?

Consult that state’s department of revenue website for taxability guides, or work with a sales tax professional. Taxability varies significantly by state and product category. Even similar items may be treated differently.

What should I do if I receive a sales tax notice from a state?

Don’t ignore it. State notices require timely responses to avoid escalating penalties. Read carefully, gather relevant documentation, and respond by the deadline. HOST’s notice management service handles these communications for clients.

How long do I need to keep sales tax records?

Most states require 3-7 years, though some require longer retention. Keep all sales records, exemption certificates, filed returns, and correspondence with tax authorities for at least the longest period required by any state where you’re registered.