Sales tax on digital products creates one of the most confusing compliance puzzles for online businesses. Unlike physical goods with decades of established rules, digital products live in a gray area where each state writes its own playbook, often in contradiction to the state next door.

Selling software subscriptions, ebooks, online courses, or streaming services? Understanding where and when to collect sales tax protects you from audits while keeping checkout friction minimal. Hands Off Sales Tax (HOST) specializes in helping digital businesses navigate multi-state obligations. From nexus analysis to automated filings, we handle the complexity so you focus on growth.

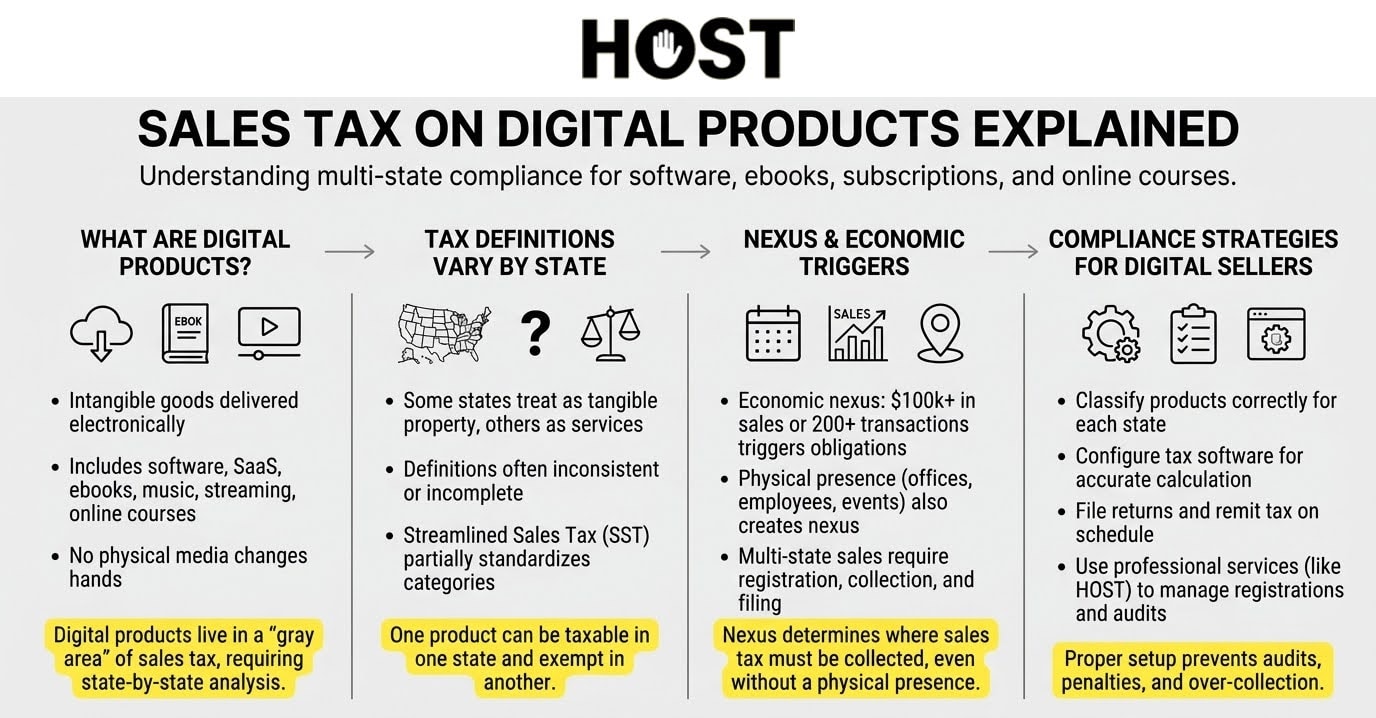

What Are Digital Products for Sales Tax Purposes?

Digital products are intangible goods delivered electronically. Downloadable software, mobile apps, ebooks, music files, streaming subscriptions, online courses, digital images, and SaaS platforms all qualify.

The defining characteristic: customers receive access through the internet, with no physical media changing hands. A customer downloading a PDF guide experiences the same transaction type as someone subscribing to cloud-based accounting software. Both are digital products.

Tax authorities categorize them inconsistently. Some states treat digital products like tangible personal property (taxable). Others consider them services (sometimes exempt). A few created specific “digital goods” categories with unique rules.

This forces businesses to analyze tax treatment state by state, product by product. What’s exempt in one jurisdiction becomes fully taxable in another.

Why Sales Tax on Digital Products Gets So Complicated

No Uniform Definition Exists

Unlike physical products where a chair remains a chair everywhere, digital products lack standardized definitions. One state might define “digital goods” to include software but exclude data. Another taxes downloaded music but exempts streamed content.

The Streamlined Sales Tax (SST) Agreement attempted standardization by creating categories like “digital automated services” and “digital audio-visual works.” Currently 24 states are full members of SST, and even within SST, variations exist in how states implement the definitions.

Physical vs. Digital Treatment Varies Wildly

Many states developed sales tax systems decades before the internet existed. Their laws reference “tangible personal property,” which is something you can touch. Digital products don’t fit this mold neatly.

The legal reasoning? Many states define tangible personal property as anything “perceptible to the senses.” Since you can see, hear, or experience digital content, states argue it qualifies as tangible, even though you can’t hold it. Arizona explicitly uses this “perceived by the senses” standard to tax digital goods.

Some states updated laws to explicitly include digital products. Others maintained that if you can’t physically touch it, it’s not taxable tangible property. The same ebook gets taxed in Texas but potentially exempted in other states that haven’t clarified digital taxation.

SaaS Gets Special Treatment

Software as a Service represents a particularly murky category. Is it a digital product, a service, or something else? States disagree violently.

New York generally exempts SaaS as a non-taxable service. Texas taxes it as data processing. Pennsylvania considers most SaaS taxable. This means a company like Salesforce must track different tax obligations for identical products depending solely on customer location.

The business model matters. Downloaded software often gets taxed as tangible personal property, while cloud-accessed software might be treated as a service. Same functionality, two completely different tax treatments.

Delivery method matters too. Some states distinguish between downloaded products (taxable as permanent purchases) versus streamed or cloud-accessed content (sometimes exempt as temporary service). Idaho and Georgia only tax digital products when buyers receive “permanent right to use,” so things like subscriptions and rentals often escape taxation entirely.

Economic Nexus Multiplied the Problem

After the 2018 South Dakota v. Wayfair decision, states gained authority to require sales tax collection based on economic activity alone. No physical presence needed. Cross a state’s threshold (typically $100,000 in sales or 200 transactions), and you must collect tax there.

For digital product sellers, this created exponential complexity. A software company with customers nationwide might trigger nexus in 30+ states simultaneously. Each state then applies its own digital product rules.

Pre-Wayfair, many digital businesses only collected tax in their home state. Post-Wayfair, they face compliance obligations in dozens of states, each with different digital product definitions.

Which States Tax Digital Products?

States That Broadly Tax Digital Products

These states explicitly tax most digital products: Alabama, Arizona, Colorado, Connecticut, District of Columbia, Hawaii, Idaho, Indiana, Iowa, Kentucky, Louisiana, Minnesota, Mississippi, Nebraska, New Jersey, New Mexico, Ohio, Pennsylvania, Rhode Island, South Dakota, Tennessee, Texas, Utah, Vermont, Washington, West Virginia, and Wisconsin.

Your ebook, software download, streaming subscription, or digital course generally triggers sales tax here. Specific exemptions exist (like educational content in some states), but the default is taxable.

States That Tax Some Digital Products

These states take a selective approach: Georgia, Illinois, Kansas, Maine, Maryland, Massachusetts, Michigan, North Carolina, North Dakota, South Carolina, and Wyoming.

Massachusetts taxes software downloads but exempts digital books and music. Illinois taxes streaming services but exempts downloaded software. Each state requires individual analysis of your specific product.

States That Generally Don’t Tax Digital Products

California, Florida, Missouri, Nevada, and Virginia either explicitly exempt digital products or have laws that don’t clearly address them.

California doesn’t tax digital products unless bundled with tangible property or services. Florida exempts digital goods delivered electronically. However, “generally don’t tax” doesn’t mean never. Specific scenarios can still trigger obligations.

States With No Sales Tax

Delaware, Montana, New Hampshire, and Oregon impose no general sales tax. Alaska has no state sales tax but allows local jurisdictions to levy their own.

This state-by-state variation means a digital product might be taxable in 27 states, exempt in 18, and somewhere in between for the remainder. HOST’s nexus analysis identifies exactly where you’ve triggered collection obligations, then maps your specific products to each state’s rules.

Common Digital Product Categories and Tax Treatment

Software and SaaS

Downloaded software faces taxation in most states that tax digital products. Cloud-based SaaS sees more variation. Some states tax it, others treat it as non-taxable service.

Custom software often receives favorable treatment. Many states exempt software created for a specific client’s unique needs, while taxing off-the-shelf software sold to multiple customers.

Streaming Services and Subscriptions

Video streaming, music streaming, and subscription access to digital content face increasing taxation. Many states now tax streaming services specifically, with more adding these provisions annually.

Some states tax streaming at different rates than other digital goods. Chicago imposes a 9% amusement tax on streaming services, which is actually higher than its standard sales tax rate.

Online Courses and Educational Content

Educational digital products occupy unique space. Many states exempt educational materials, but the definition of “educational” varies dramatically.

An online course offered by an accredited institution might be exempt. The same content offered by a business coaching platform could be taxable. Some states require educational exemptions to be tied to degree programs or certified curricula.

Bundled Digital and Physical Products

Selling digital products alongside physical goods creates complexity. Many states tax the entire bundle if it includes any taxable component. A digital subscription bundled with a printed book becomes taxable on the full amount in most jurisdictions.

Minnesota considers a bundle taxable unless the taxable portion represents 10% or less of the total price. Separate your pricing clearly in transactions to avoid overcharging customers and simplify compliance.

How to Handle Sales Tax Compliance for Digital Products

Determine Where You Have Nexus

Identify every state where you’ve exceeded economic nexus thresholds. Track sales revenue and transaction counts by state monthly. Once you cross a state’s threshold, you’ve triggered a collection obligation.

Physical presence still creates nexus. Employees, offices, warehouses, or trade shows in a state establish nexus, requiring you to collect tax on all sales there, including digital products.

Register in Required States

Once you’ve identified nexus states and know which products are taxable where, register for sales tax permits. Each state requires separate registration, with varying documentation and processing times.

Some states issue permits immediately. Others take 4-6 weeks. Late registration can result in back-tax assessments and penalties.

HOST handles registrations in all required states, managing paperwork, follow-up, and state communications so you get compliant quickly.

Configure Tax Software Correctly

Sales tax automation tools like TaxJar or Avalara calculate tax at checkout, but they require proper configuration. You must set up product mappings, nexus settings, and exemption certificates.

Misconfiguration causes serious problems. Common errors include taxing exempt products, applying wrong rates, or failing to collect where required.

HOST offers a Free Sales Tax Software Review to audit your existing configuration and identify costly errors before they impact your bottom line.

File Returns and Remit Tax

Every state where you’re registered requires periodic filing monthly, quarterly, or annually. Returns must be filed even if you collected zero tax.

Miss a filing deadline and penalties accumulate quickly. Managing filings across 20+ states means tracking dozens of different due dates, forms, and requirements.

HOST’s automated filing service handles all returns across all jurisdictions, ensuring everything stays current while freeing your time for revenue-generating activities.

HOST: Your Partner for Digital Product Sales Tax Compliance

Sales tax on digital products is constantly evolving as states modernize tax codes for the digital economy. Managing compliance across dozens of jurisdictions while running a digital business diverts crucial time and resources from growth.

What HOST Delivers:

Nexus Analysis: We determine exactly where you have collection obligations based on your sales footprint across all states and product types.

Product Classification: We analyze how each state treats your specific digital products, creating a comprehensive taxability matrix.

Sales Tax Registration: We handle registrations in all required states, managing paperwork and state communications.

Automated Filing: We file your returns across all jurisdictions monthly, quarterly, or annually, keeping everything current.

Software Optimization: We review and optimize your TaxJar, Avalara, or other automation tools to calculate correctly for digital products.

Notice Management: We interpret and respond to state notices, protecting you from penalties while resolving issues efficiently.

Audit Defense: We’re your trusted partner in resolving your sales tax audit, organizing documentation and defending your position.

Voluntary Disclosure Agreements: If you discover past obligations, we file VDAs with states to limit lookback periods and abate penalties.

We’ve been 100% focused on sales tax since 1999. That’s over 25 years helping businesses navigate compliance complexities. Founded by Mike Espenshade, with parent company TaxMatrix serving North America’s largest companies, we bring enterprise expertise to digital businesses of all sizes.

Ready to Simplify Your Digital Product Tax Compliance?

Digital product sales tax doesn’t have to be an ongoing headache. The right compliance partner ensures you collect correctly in every jurisdiction without constant worry about changing rules or missed deadlines.

Whether you’re just crossing economic nexus thresholds, expanding your digital product line, or discovering past obligations, professional help eliminates guesswork and prevents costly mistakes.

Contact HOST today to discuss your compliance needs or schedule a free consultation. Let us handle the tax so you can focus on sales.

Want to learn more? Get our “10 Sales Tax Mistakes E-Commerce Sellers Make” e-book.

Frequently Asked Questions

Are digital products subject to sales tax?

It depends on the state and product type. Many states broadly tax digital products, while others tax selectively or exempt them entirely. SaaS, ebooks, streaming services, and software each face different treatment across jurisdictions, requiring state-by-state analysis.

How do I know if I need to collect sales tax on my digital products?

First, determine where you have nexus (physical presence or economic nexus via $100,000+ in sales). Then research how each nexus state treats your specific digital product category. If a state taxes your product type and you have nexus there, you must collect.

Is SaaS taxable?

SaaS taxability varies dramatically by state. Texas, Pennsylvania, and Washington tax most SaaS. New York generally exempts it as a non-taxable service. Many states have specific SaaS taxation rules, with treatment depending on whether the software fits each state’s definition of taxable services or digital products.

Do I charge sales tax based on my location or my customer’s location?

Sales tax applies based on your customer’s location (destination-based sourcing). A Texas customer pays Texas sales tax rates if the product is taxable in Texas, regardless of where your business is located. You must track customer addresses and apply appropriate jurisdiction rates.

What happens if I haven’t been collecting sales tax on digital products?

Uncollected sales tax creates liability. You owe the tax even if you didn’t collect it from customers. States can audit back 3-4 years (sometimes longer), assessing back taxes plus penalties and interest. Voluntary Disclosure Agreements (VDAs) can limit lookback periods and reduce penalties if you come forward proactively.

Do B2B digital product sales get taxed differently than B2C?

Sometimes. Iowa exempts digital products sold to commercial enterprises using them exclusively for business purposes. South Carolina offers commercial exemptions under specific conditions. Other states make no distinction, taxing all digital sales regardless of buyer type.

If you sell primarily to businesses, research B2B exemptions in your nexus states. Proper documentation (resale certificates, exemption forms) is critical. These exemptions could significantly reduce your tax obligations, but claiming them incorrectly triggers audit risk.

How often do digital product tax laws change?

Digital product sales tax laws change frequently as states modernize tax codes for the digital economy. Arkansas expanded taxation to include streaming services in 2023. Georgia clarified “permanent use” rules in January 2024. Louisiana expanded digital taxation in January 2025.

Multiple states update digital taxation rules annually. Without ongoing monitoring, businesses often discover they’re out of compliance when laws change. Professional management includes tracking legislative developments and adjusting compliance accordingly.