Understanding Maine sales tax nexus matters when you’re selling to customers in The Pine Tree State. Cross Maine’s threshold, and you’re suddenly responsible for registration, collection, and ongoing filings that don’t pause for busy seasons or staffing shortages.

From economic triggers to physical presence rules, the right compliance partner ensures you collect correctly without drowning in administrative work. Hands Off Sales Tax (HOST) specializes in multi-state nexus analysis, registration, and filings, helping you stay compliant in Maine and across all 45 sales tax states.

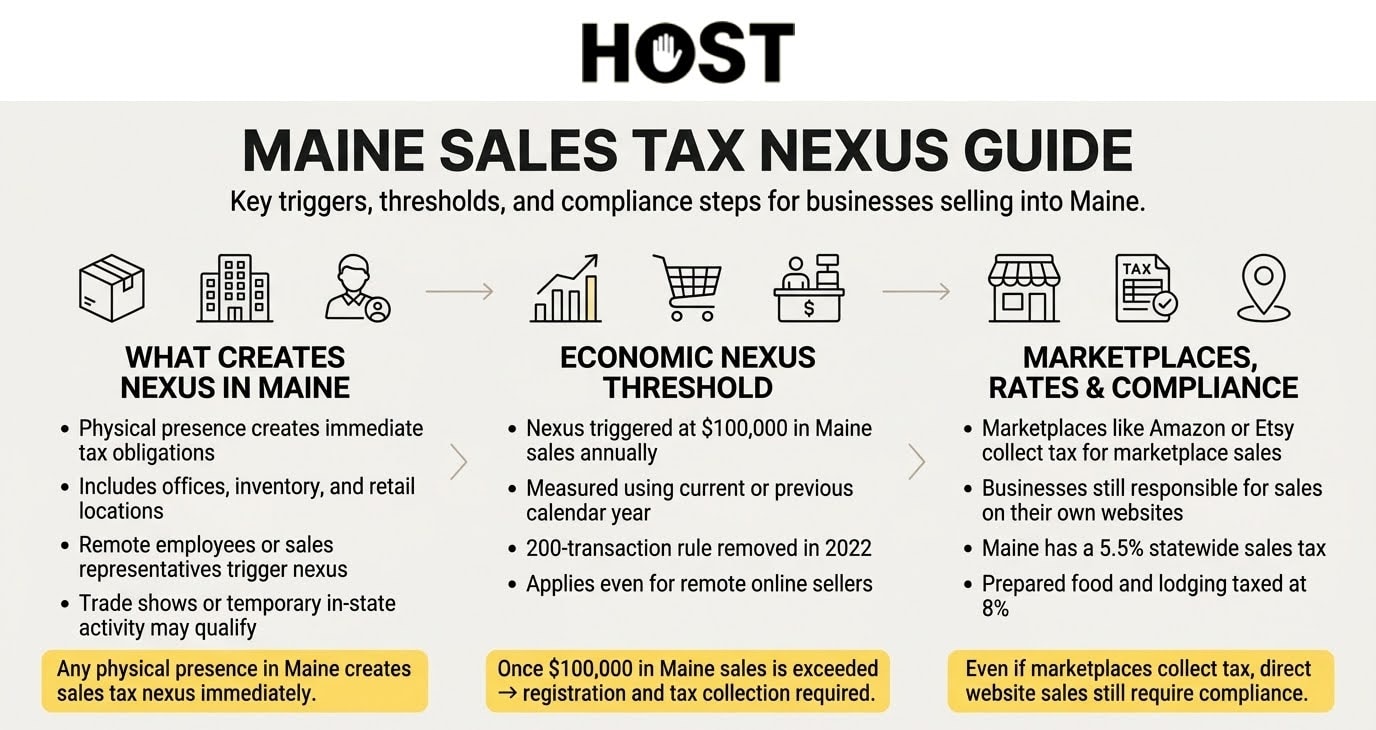

What Is Sales Tax Nexus?

Sales tax nexus is the connection between your business and a state that creates a legal obligation to collect and remit sales tax. Think of it as the threshold that transforms you from an out-of-state seller into a business with tax responsibilities in Maine.

The 2018 South Dakota v. Wayfair Supreme Court decision fundamentally changed nexus rules. Before Wayfair, only physical presence triggered nexus. After Wayfair, states gained authority to require remote sellers to collect tax based solely on economic activity.

Your Maine sales tax nexus can now be triggered entirely through online transactions, even if you’ve never visited Portland or Bar Harbor.

Maine Economic Nexus Rules

Maine adopted economic nexus on July 1, 2018, immediately following Wayfair. The state requires remote sellers to collect and remit sales tax once they exceed a specific threshold.

Maine’s economic nexus threshold: $100,000 in gross sales delivered to Maine during the previous or current calendar year.

Note: Maine eliminated its 200-transaction threshold effective January 1, 2022, simplifying compliance for sellers with many small transactions.

Once exceeded, remote sellers must register and begin collecting on the first day of the first month that begins at least 30 days after crossing the threshold. Cross $100,000 in June? Collection starts August 1.

HOST’s nexus analysis service examines your sales data across all states, identifying exactly when and where you’ve met thresholds, preventing the common mistake of discovering obligations months or years late.

Physical Nexus in Maine

Physical nexus still triggers sales tax obligations immediately, regardless of sales volume. Physical presence creates nexus from day one.

Physical nexus triggers in Maine:

- Inventory: Goods stored in Maine warehouses, fulfillment centers, or third-party facilities

- Offices or retail locations: Any leased or owned physical space

- Employees: Workers living in Maine, including remote employees or salespeople

- Temporary presence: Attending trade shows or pop-up retail events

- Affiliates: Related businesses with Maine presence that refer customers

The inventory trigger matters for FBA sellers. If Amazon stores your products in a Maine fulfillment center, you’ve established physical nexus. Even if Amazon chose that location without your input.

Similarly, hiring one remote employee who lives in Portland creates immediate physical nexus. That customer service representative just triggered your Maine sales tax obligations.

Affiliate and Click-Through Nexus

Maine also recognizes affiliate nexus when you have relationships with Maine-based businesses. If an affiliated company in Maine sells similar products, shares your branding, or facilitates deliveries for your business, you may have nexus even without direct physical presence.

Click-through nexus triggers when Maine-based affiliates refer customers to you (through website links, social media, or other methods) and those referrals generate more than $10,000 in sales over the preceding 12 months. This catches many businesses using affiliate marketing programs or influencer partnerships.

Physical nexus is immediate and retroactive. Discovered inventory in Maine for six months? You technically should have been collecting tax those entire six months. This is where Voluntary Disclosure Agreements (VDAs) become valuable, limiting lookback periods and waiving penalties.

Marketplace Facilitator Laws

Maine enacted marketplace facilitator legislation on October 1, 2019, significantly changing obligations for sellers using platforms like Amazon, eBay, or Etsy.

How it works: Marketplace facilitators collect and remit sales tax on behalf of third-party sellers for sales made through the platform.

What this means for you:

- Amazon FBA sales: Amazon handles Maine sales tax

- Etsy sales: Etsy manages collection and remittance

- Your own website: You’re responsible for Maine sales tax if you have nexus

This creates dual compliance for many businesses. Your marketplace sales are covered, but direct website sales require separate compliance.

Important limitation: Marketplace facilitator laws don’t eliminate your nexus. They simply shift collection responsibility. You still technically have nexus in Maine, which could matter for other taxes or regulatory requirements.

HOST helps businesses navigate this complexity, ensuring correct collection across all channels while avoiding gaps in compliance.

How to Register for Maine Sales Tax

Once you’ve established Maine sales tax nexus, registration is mandatory before collecting your first dollar.

Maine registration process:

Gather required information: FEIN or SSN, business legal name and DBA, physical address, ownership structure, NAICS code, and estimated monthly Maine sales.

Register online: Maine Revenue Services provides registration through the Maine Tax Portal. The process typically takes 15-30 minutes with information prepared.

Receive your certificate: Maine issues a Sales and Use Tax Certificate of Registration with your account number, usually within 7-10 business days. You cannot legally collect sales tax until you receive this certificate.

Understand filing frequency: Maine assigns monthly, quarterly, or annual filing based on estimated tax liability. Most remote sellers start quarterly, though high-volume sellers may receive monthly assignments.

Common registration mistakes include registering late after exceeding thresholds, using incorrect business entity information, and not understanding filing frequency assignments.

HOST handles Maine sales tax registration completely. Managing paperwork, follow-up, and ensuring correct setup.

Maine Sales Tax Rates and Taxability

Maine sales tax rates:

- Standard rate: 5.5% on most tangible personal property

- Prepared food and lodging: 8% on restaurant meals, prepared food, and short-term lodging

- No local taxes: Maine has no local sales taxes, simplifying compliance

Maine uses destination-based sourcing, meaning you charge tax based on where your customer receives the product, not where your business is located.

Taxable in Maine: Most tangible personal property, prepared food and restaurant meals (8%), lodging (8%), most services, and digital products (downloadable software, apps, e-books, streaming services).

Exempt in Maine: Groceries (unprepared food), prescription medications, certain medical devices, seeds and agricultural items, and manufacturing equipment.

Clothing note: Unlike Massachusetts, Maine does not exempt clothing from sales tax. All clothing and footwear are taxable at 5.5%.

Shipping charges: Not taxable if separately stated on the invoice and shipped via carrier or U.S. mail. However, if shipping costs are included in the product price, the entire amount becomes taxable.

For e-commerce sellers, digital products represent a significant compliance area. Maine taxes digital audio, audiovisual works, and books. Streaming subscriptions included.

Correctly configuring your sales tax software to apply Maine’s 5.5% rate only to taxable items prevents problems. Overcollecting frustrates customers; undercollecting creates audit liability.

HOST’s Free Sales Tax Software Review audits your TaxJar, Avalara, or other automation setup to identify configuration errors before they cost you money.

Filing Maine Sales Tax Returns

Once registered, you must file Maine sales tax returns according to your assigned frequency, even if you made no Maine sales during the period.

Filing deadlines: Returns are due on the 15th day of the month following the reporting period. January’s sales are due February 15.

What’s reported: Total gross sales, exempt sales (with documentation), taxable sales, total tax collected, and any use tax owed.

Zero returns: Even with no tax collected, you must file a zero return by the deadline. Failing to file creates penalties, even when no tax is owed.

Common filing mistakes: Missing deadlines (10% penalty plus interest), reporting wholesale sales as taxable, failing to remit collected tax, and not filing required zero returns.

The penalty for late filing is 10% of tax due or $25, whichever is greater. Interest accrues daily on unpaid balances at Maine’s statutory rate.

HOST handles all Maine sales tax filings (monthly, quarterly, or annually) ensuring deadlines are never missed and returns are accurately prepared.

Voluntary Disclosure Agreements for Maine

Discovered you’ve had Maine nexus for months or years without collecting tax? A Voluntary Disclosure Agreement resolves past liabilities while minimizing penalties.

VDA benefits:

- Limited lookback: Typically 3 years instead of the full 6-year statute

- Penalty waiver: Maine waives failure-to-register and failure-to-file penalties

- Anonymity during negotiation: Initial disclosure can be anonymous until terms are agreed

When to consider a VDA: You discovered past nexus but never registered, an audit notice arrived, you’re cleaning up compliance before a business sale, or you’re expanding into Maine and want to clear historical issues.

The VDA process typically takes 60-90 days from initial submission to completion. Maine Revenue Services generally cooperates with businesses making good-faith compliance efforts.

Cost-benefit: While you’ll pay back taxes for the lookback period, penalty savings often exceed 10-25% of the liability. For a business with $50,000 in uncollected Maine tax over 6 years, penalty savings could reach $5,000-$12,500.

HOST manages voluntary disclosures with Maine, negotiating favorable terms and handling all documentation.

Stay Compliant: HOST Handles Maine Sales Tax

Maine sales tax nexus creates immediate obligations that never stop. Missing deadlines or miscalculating tax creates audit risk small businesses can’t afford.

What HOST delivers:

- Nexus Analysis: We determine exactly when you established Maine nexus

- Registration Services: We handle complete Maine registration and state communications

- Ongoing Filings: We prepare and file your returns monthly, quarterly, or annually. Always on time

- Software Optimization: We review your tax software configuration for correct Maine calculations

- Notice Management: We interpret and respond to Maine Revenue Services notices

- Audit Defense: We organize documentation and defend your position in audits

- VDA Services: We negotiate voluntary disclosures when past nexus is discovered

We’ve been 100% focused on sales tax since 1999. That’s over 25 years helping e-commerce businesses navigate compliance in Maine and all 44 other sales tax states. Founded by Mike Espenshade, with parent company TaxMatrix serving North America’s largest companies, we bring enterprise expertise to businesses of all sizes.

You handle the sales, we handle the tax.

Ready to Get Maine Compliant?

Understanding when you’ve triggered Maine sales tax nexus is the first step. Taking action before penalties accumulate is the second. Whether approaching the $100,000 threshold, discovering past nexus, or wanting expert management of ongoing compliance, professional help eliminates guesswork.

At HOST, we combine deep sales tax expertise with transparent communication and personalized support. Every business receives dedicated attention, from initial nexus analysis through ongoing multi-state filings.

Contact HOST today to discuss your Maine sales tax needs or schedule a free consultation. Let us handle Maine compliance so you can focus on growth.

Want to learn more? Get our “10 Sales Tax Mistakes E-Commerce Sellers Make” e-book.

Frequently Asked Questions

What triggers sales tax nexus in Maine?

Maine sales tax nexus is triggered by either economic activity ($100,000 in sales) or physical presence (inventory, employees, offices) in the state. Both create immediate registration and collection obligations.

Do I need to collect Maine sales tax on digital products?

Yes. Maine taxes digital audio works, audiovisual works, and books at the standard 5.5% rate. This includes streaming subscriptions, downloadable software, e-books, and apps.

Is shipping taxable in Maine?

Shipping charges are not taxable if separately stated on your invoice and shipped via common carrier or U.S. mail. However, if you include shipping in your product price without separating it, the entire amount becomes taxable.

How long do I have to register after establishing Maine nexus?

Collection must begin the first day of the first month that begins at least 30 days after exceeding the threshold. Best practice is to register immediately upon crossing $100,000.

Does Maine have local sales taxes?

No. Maine has a single statewide rate of 5.5% (8% for prepared food and lodging) with no local option taxes, making Maine one of the simpler states for rate calculation and compliance.

What happens if I’ve been selling in Maine without collecting tax?

You’re technically liable for uncollected tax. A Voluntary Disclosure Agreement can limit lookback periods to 3 years and waive penalties, significantly reducing exposure compared to waiting for an audit.

How often do I need to file Maine sales tax returns?

Maine assigns filing frequencies based on tax liability. Monthly for high-volume sellers, quarterly for most remote sellers, and annually for minimal activity. You must file by the 15th of the month following each period, even with no tax collected.