Understanding Virginia sales tax on services means decoding one of the trickier corners of state tax law. Most services slide through tax-free, but specific categories like accommodations, communications, anything involving tangible goods trigger obligations that catch businesses off guard.

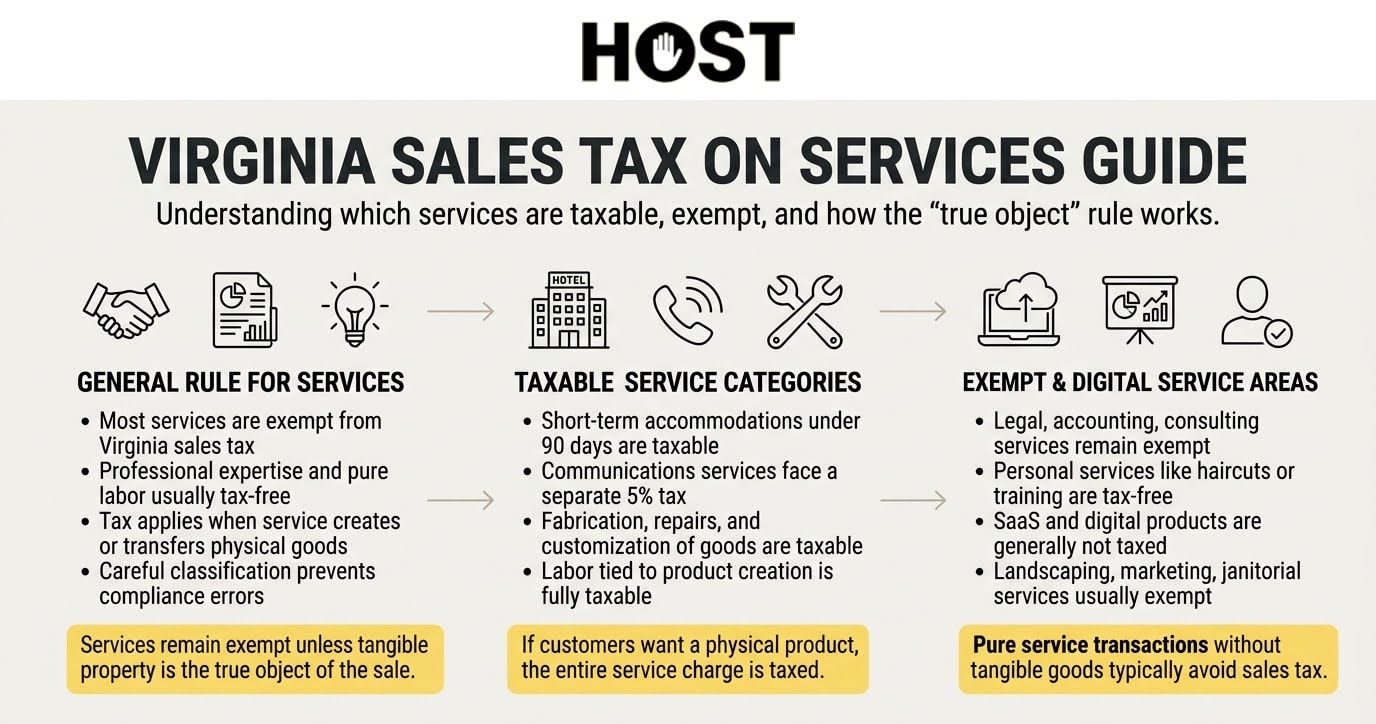

The general rule sounds deceptively simple: services are exempt unless they involve physical property or fall into explicitly taxable buckets. Reality demands scrutinizing what you’re actually selling, how it’s delivered, and whether your service creates or transfers something tangible.

For businesses managing multi-state obligations, HOST handles the heavy lifting. Nexus analysis, registration, filing, and audit defense so you can focus on growth instead of tax code archaeology.

The Foundation: Services Walk Free

Virginia law establishes that service charges are generally exempt from retail sales and use tax. Professional expertise, consulting, pure labor, these typically don’t trigger collection requirements.

The catch? Services creating or manufacturing products may require collecting tax on those products.

This distinction creates the compliance minefield: determining whether your transaction qualifies as exempt service or taxable sale wrapped in service packaging.

The “True Object” Test Decides Everything

Virginia uses the “true object” test for transactions mixing services and tangible property.

What’s the customer actually buying?

When the service itself is the goal and physical property is incidental, the transaction stays exempt. When customers want the physical product your service produces, the entire charge becomes taxable. Services included.

Exempt Service Example: A CPA prepares your taxes and delivers reports digitally. The true object is professional expertise. Those reports merely document the service rendered. Exempt.

Taxable Sale Example: You commission a custom portrait. Despite the artist’s considerable labor, the entire transaction gets taxed because customers want the physical painting.

When transactions blend both elements, determining taxability requires analyzing what customers primarily seek. Product incidental to expertise? Likely exempt. Product itself? Tax applies to everything.

Taxable Services in Virginia

While most services escape Virginia sales tax, several categories create definite obligations.

Accommodations Under 90 Days

Hotel rooms, campground spaces, and short-term lodgings face Virginia sales tax on the total charge. The tax applies to transients like guests staying fewer than 90 continuous days.

Additional charges bundled with accommodations such as movies, Wi-Fi, parking, resort fees become taxable as part of the room charge.

Booking Platforms: Airbnb, Vrbo, and hotel booking sites must collect Virginia sales tax on service fees plus room charges. Many Virginia localities pile additional transient occupancy taxes (2-10%) onto the state rate.

Communications Services Get Their Own Tax

Virginia imposes separate 5% communications sales tax on telecommunications including phone service (landline, wireless, VoIP), cable television, and satellite TV and radio.

Not Taxed: Over-the-air broadcasts, equipment installation, or equipment sales (which may face regular sales tax separately).

Businesses providing telecommunications must register separately for communications sales tax and file monthly by the 20th.

Services Tied to Tangible Property

Services connected to tangible personal property sales are taxable, including fabrication services whether customers supply materials or not.

Manufacturing and Fabrication: Custom metalwork, furniture building, garment tailoring, anything creating physical products from raw materials becomes fully taxable on materials and labor.

Repair and Modification: Fixing tangible property triggers sales tax on the full service charge. Smartphone screen replacement, laptop repair, appliance installation, all taxable.

Customization Services: Engraving jewelry, monogramming clothing, upgrading computer hardware, these alterations create taxable transactions.

The dividing line often depends on who provides materials. When your business supplies materials and transforms them into finished products, the transaction becomes taxable regardless of labor intensity.

Services Remaining Exempt

Virginia maintains broad exemptions for pure service transactions avoiding tangible property.

Professional Services: Legal, accounting, consulting, architectural, engineering, and medical services remain exempt. Transactions focused on expertise rather than delivering physical products.

Personal Services: Haircuts, dry cleaning, personal training stay tax-free. Even though salons use products, the true object is service itself.

Business Services: Janitorial, landscaping, advertising, marketing, and property management generally remain exempt.

Software as a Service: SaaS is non-taxable in Virginia. The state doesn’t tax cloud services, SaaS, or digital products. Only physical goods and specifically enumerated services.

This creates advantages for technology companies and subscription services compared to states aggressively taxing digital offerings.

Gray Areas Demanding Attention

Several scenarios create confusion and compliance risks.

Quick Reference: Common Services and Their Tax Status

| Service Type | Taxable? | Why |

| Legal advice, accounting | Exempt | Professional services, no tangible property |

| Portrait painting, custom art | Taxable | Customer wants physical product |

| Haircuts, dry cleaning | Exempt | Personal services, true object is service |

| Smartphone repair | Taxable | Service to tangible property |

| Graphic design (digital delivery) | Exempt | Service producing digital files |

| Graphic design (printed materials) | Taxable | Customer wants physical product |

| IT consulting | Exempt | Pure advisory service |

| Software installation | Taxable | Service to tangible property |

| Landscaping services | Exempt | Service, not product transfer |

Mixed Transactions

Selling tangible property and exempt services together requires careful analysis. Transactions involving both generally are taxable or exempt on the full amount, regardless of separate line items.

The true object test determines outcomes. Customers primarily want the product? The entire charge becomes taxable. Purchasing service with incidental product? May stay exempt.

Example: A designer creates custom logos. If customers purchase design expertise and happen to receive files, this might be exempt. If customers contract for physical banners featuring the logo, the entire transaction becomes taxable since the tangible good is the object.

Document Services: A business provides fax transmission services. The service itself is exempt. But if they charge separately for copies of faxed documents, those copy charges become taxable. The transmission is service; the copies are tangible property.

Information on Physical Media

Information on tangible media (diskettes, reports, CDs) generally is taxable except for information customized to one customer’s specific needs.

Market research sold identically to multiple clients on CDs? Taxable. Customized analysis for a single client delivered digitally or on paper? Exempt.

Digital Products and Downloads

Virginia takes a taxpayer-friendly approach: digital goods are not taxable. This means ebooks, downloaded software, digital music, online courses, and digital art all remain exempt.

The distinction between digital products (exempt) and tangible products delivered digitally requires careful analysis of what you’re actually selling.

Multi-State Complications

Even service-based businesses face Virginia nexus under specific circumstances.

Economic Nexus Threshold

Effective July 1, 2019, Virginia considers businesses with $100,000 or more in Virginia sales, or 200 or more separate transactions, to have economic nexus.

This threshold applies regardless of what you sell. Exempt services generating $100,000+ in Virginia revenue still cross economic nexus, which is certainly relevant if you also sell taxable goods or services.

Service Businesses Purchasing Property

Service providers purchasing tangible property for use in providing exempt services are taxable users and consumers of that property. If suppliers don’t collect tax, service providers must remit use tax directly.

A landscaping company purchasing equipment for exempt landscaping services owes sales or use tax on equipment purchases, even though services provided remain exempt.

Registration Reality: Even if your services are entirely exempt, you must register for sales tax collection if you also sell ANY taxable items, even occasionally. Service providers who occasionally sell products alongside exempt services need full registration and filing obligations.

New Filing Requirements

Starting with April 2025 filing periods, all Virginia sales tax filers use Form ST-1, which replaced previous forms (ST-9, ST-8, ST-7, ST-6). Service businesses now registered must use this unified form for all returns, simplifying the filing process across different business types.

HOST: Clarity on Virginia Service Taxability

Determining whether services trigger Virginia collection requires analyzing each transaction type and properly documenting distinctions between taxable and exempt elements.

What HOST Delivers:

Nexus Analysis: We analyze your Virginia footprint to determine whether you’ve triggered economic or physical nexus thresholds, examining taxable and exempt revenue.

Service Taxability Review: We evaluate specific offerings to determine which create Virginia obligations and which remain exempt, providing clear guidance on mixed transactions.

Multi-State Registration: We handle registration with Virginia and all required states, managing paperwork so you’re collecting correctly everywhere.

Ongoing Compliance: HOST files your returns monthly, quarterly, or annually based on Virginia’s requirements, ensuring timely remittance and proper reporting.

Audit Defense: If Virginia questions your determinations, we handle communications with tax authorities, prepare documentation, and defend your position.

Notice Management: We interpret and respond to Virginia Department of Taxation notices, resolving issues before they escalate.

Founded in 1999, HOST has specialized exclusively in sales tax compliance for over 25 years. Through parent company TaxMatrix, we’ve helped North America’s largest companies navigate complex multi-state obligations. Expertise we now bring to growing service businesses.

Ready to Simplify Virginia Compliance?

Service taxability in Virginia requires analyzing what you’re selling, how you’re delivering it, and whether the true object involves tangible property. One misclassification creates years of back taxes, penalties, and interest.

Whether expanding service offerings into Virginia, unclear about mixed transactions, or managing compliance across states, professional guidance eliminates guesswork and prevents costly mistakes.

Contact HOST today to discuss your Virginia obligations or schedule a free consultation. Let us handle the complexity so you can focus on growing your service business.

Frequently Asked Questions

Are most services taxable in Virginia?

No. Services are generally exempt from retail sales and use tax in Virginia. However, services connected to tangible personal property sales become taxable.

What types of services are taxable in Virginia?

Accommodations (hotels, short-term rentals under 90 days), communications services (phone, cable, VoIP), and services creating or modifying tangible personal property are taxable.

How do I know if my service is taxable or exempt?

Virginia uses the “true object” test. If customers want service and tangible property is incidental, the transaction may be exempt. If customers want the physical product your service creates, the entire charge becomes taxable.

Is SaaS taxable in Virginia?

No, SaaS is non-taxable in Virginia. The state doesn’t tax cloud services, SaaS, or digital products. Only physical goods and specifically enumerated services.

Do I need to collect Virginia sales tax if I only provide services?

It depends! If services remain genuinely exempt and you don’t sell taxable goods, you likely don’t collect Virginia sales tax. However, once you exceed $100,000 in Virginia sales or 200 transactions, you establish economic nexus. If you later add taxable offerings, collection obligations begin immediately.

What should I do if I’m unsure whether my service is taxable?

Seek professional guidance before making taxability determinations. Misclassifying taxable services as exempt creates liability for uncollected tax plus penalties and interest. HOST provides consultation services to evaluate specific offerings and deliver clear taxability guidance.