Sales tax on prescription drugs remains one of the most consistent exemptions across the United States, offering critical relief to consumers managing healthcare costs. For e-commerce sellers, pharmacy operators, and retailers selling medication across multiple states, understanding these exemptions is about avoiding costly mistakes that can trigger audits and penalties.

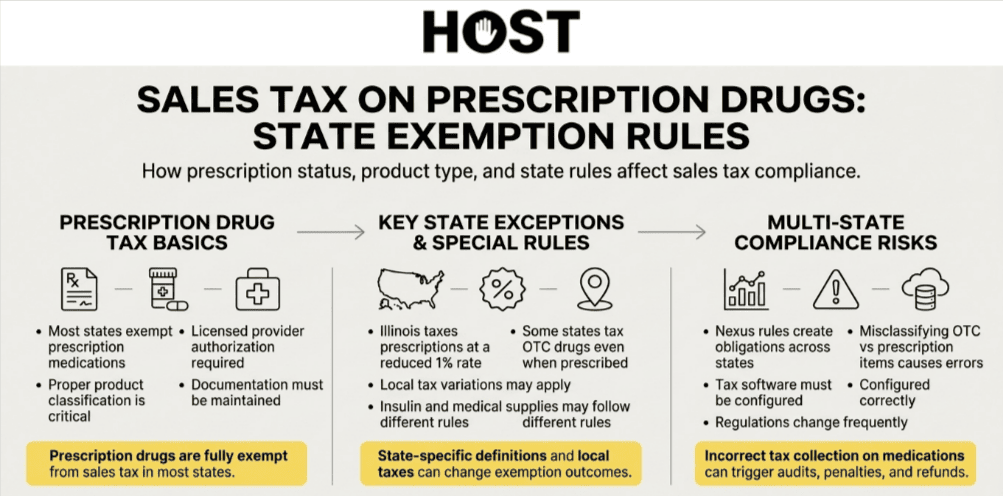

The landscape is simpler than most sales tax scenarios: 44 of 45 states with sales tax exempt prescription drugs entirely. Illinois stands alone, taxing prescriptions at a reduced 1% rate. Yet beneath this apparent simplicity lies a complex web of definitions, special circumstances, and state-specific rules that can trap the unprepared.

That’s where Hands Off Sales Tax (HOST) helps businesses navigate the nuances. Through comprehensive nexus analysis and state-specific research, we ensure you’re collecting correctly, never overtaxing exempt medications or missing obligations where they exist.

Understanding Prescription Drug Tax Exemptions

Prescription drugs benefit from widespread tax exemptions because lawmakers recognize healthcare as a fundamental need. Unlike discretionary purchases, medications prescribed by licensed healthcare providers receive special treatment in state tax codes. This distinction makes them significantly more affordable than over-the-counter alternatives.

For retailers and e-commerce sellers, this creates a critical compliance requirement. You must distinguish between prescription and non-prescription medications accurately. The difference determines whether you collect tax at checkout, and mistakes in either direction create problems. Overtaxing prescriptions damages customer relationships and can trigger refund demands. Undertaxing non-exempt items leaves you liable for uncollected tax during audits.

The federal government provides the foundation: prescription drugs dispensed by licensed pharmacists on written prescription from authorized healthcare providers qualify for exemption. However, each state interprets and implements this principle differently. What counts as a “medicine,” which healthcare providers can write qualifying prescriptions, and how documentation must be maintained all vary by jurisdiction.

Understanding these state-specific rules is essential for multi-state compliance. A medication exempt in California might face different treatment in Georgia or Louisiana. For businesses operating across state lines, this complexity multiplies with each new market entered.

The National Landscape of Prescription Drug Exemptions

Across the United States, prescription drug exemptions operate on a consistent principle: medications prescribed by licensed healthcare providers and dispensed by authorized pharmacists receive favorable tax treatment. This reflects a national consensus that healthcare costs should not be artificially inflated through taxation on essential medications.

The scope of exemption typically covers drugs listed in the United States Pharmacopeia, Homeopathic Pharmacopeia, or National Formulary, federal standards that define what constitutes a legitimate drug. States reference these authorities to determine which substances qualify as medicines. This creates baseline consistency while allowing states to adopt their own definitions for edge cases.

However, definitions matter significantly when determining taxability. The distinction between a “medicine” and other ingestible substances varies by state. Some jurisdictions exempt vitamins and dietary supplements when prescribed. Others tax them regardless of prescription status. Herbal preparations, compounded medications, and combination products can fall into gray areas requiring state-specific research.

The FDA Drug Facts label plays a crucial role in many states. Products bearing this label (indicating FDA recognition as drugs) often receive automatic exemption when prescribed. Products without this designation may face tax even with a prescription, depending on the state.

For businesses navigating these complexities, HOST’s nexus analysis and state-specific research services provide clarity. We determine exactly where your products face tax obligations and configure your systems to handle state-by-state variations correctly.

State-by-State Breakdown of Prescription Drug Exemptions

States with Universal Prescription Drug Exemptions

The overwhelming majority of states provide blanket exemptions for prescription medications filled at licensed pharmacies. This includes major selling states that e-commerce businesses frequently encounter:

Large Market States: California, Florida, New York, and Texas all exempt prescription drugs entirely. These four states alone represent massive portions of most sellers’ customer bases, and all provide clear exemptions for prescribed medications dispensed by pharmacists.

Additional Major States: Maryland, Minnesota, Connecticut, Vermont, Pennsylvania, New Jersey, and Virginia join the universal exemption states. Most other states with sales tax follow this same pattern.

In these jurisdictions, compliance is straightforward: prescription drugs don’t get taxed. Your sales tax software should be configured to recognize prescription drug SKUs and apply zero tax. The challenge lies in maintaining proper documentation proving prescription status in case of audit.

The Illinois Exception

Illinois operates differently from every other state, creating a unique compliance requirement for sellers serving Illinois customers.

Illinois charges a reduced 1% state tax on prescription drugs, compared to its standard 6.25% rate. While this represents substantial savings for consumers, it creates complexity for retailers. You must configure systems to apply the correct reduced rate rather than full tax or zero tax.

Importantly, Illinois local jurisdictions cannot tax prescription drugs. This means prescription medications face only the 1% state rate without additional county or city taxes. For multi-state sellers, Illinois requires special attention in your tax automation setup to avoid calculation errors.

Special Circumstances and Nuances

Several states have carved out exceptions or limitations that create compliance challenges:

Georgia’s OTC Rule: Georgia exempts prescription medications but taxes over-the-counter drugs, even when purchased under prescription. This unusual rule means a customer cannot convert an OTC medication into a tax-exempt purchase simply by obtaining a prescription. For sellers, this requires distinguishing not just prescription status but whether the underlying product is inherently OTC.

Louisiana’s Parish Taxes: Louisiana provides no state-level tax on prescription drugs, but many parishes (Louisiana’s county equivalent) impose local sales taxes on prescriptions. This creates a patchwork where prescription taxability depends on precise customer location within the state. For businesses, this demands address-level tax validation for Louisiana customers.

South Carolina and Hawaii Hospital Limitations: Both states generally exempt prescription drugs but limit exemptions to direct patient sales. Hospitals, clinics, and medical facilities purchasing prescription drugs for patient care may owe tax on their purchases in these states. For pharmaceutical distributors selling to institutions, this creates different obligations than retail pharmacy sales.

These special circumstances demonstrate why relying on general rules creates risk. HOST’s state-specific research identifies these edge cases and ensures your compliance strategy accounts for each state’s unique requirements.

Over-the-Counter Medications: A Different Story

Over-the-counter medications face dramatically different tax treatment than prescriptions. While prescription drugs enjoy near-universal exemption, OTC drugs are taxable in most states.

Taxable in Most States: Forty-one states tax OTC medications at their standard sales tax rates. Consumers buying pain relievers, cold medicine, antacids, and similar products without prescriptions pay full sales tax in these jurisdictions.

States Exempting OTC Drugs: Nine states and the District of Columbia provide exemptions for over-the-counter medications: Connecticut, Florida, Maryland, Minnesota, New Jersey, New York, Pennsylvania, Texas, Vermont, and Virginia. In these jurisdictions, consumers can purchase OTC medications tax-free even without prescriptions.

Texas’s Drug Facts Requirement: Texas provides an instructive example of how states define exemptions. To qualify for tax exemption in Texas, OTC products must display FDA Drug Facts labeling. This label indicates FDA recognition of the product as a drug rather than a cosmetic or supplement. Products without this designation face tax regardless of medical use.

The Prescription Conversion: In most states that tax OTC medications, obtaining a prescription from a healthcare provider renders the product exempt. A customer purchasing Claritin-D over the counter pays tax, but the same customer with a prescription for Claritin-D receives the medication tax-free. This principle applies broadly but not universally, with Georgia being the notable exception.

For retailers, this creates inventory challenges. The same SKU may be taxable or exempt depending on whether the customer has a prescription. Point-of-sale systems must be configured to handle this distinction, and documentation requirements increase to prove exemption claims.

Insulin’s Special Status: Insulin occupies a unique position in tax law due to its essential nature for diabetics. All states except Illinois exempt insulin on prescription. Illinois applies its 1% reduced rate to prescription insulin rather than full exemption. Many states go further, exempting non-prescription insulin and diabetes testing supplies. Though significant exceptions exist in California, Connecticut, Florida, Hawaii, Illinois, Kansas, Kentucky, Louisiana, Massachusetts, New Mexico, North Dakota, Utah, West Virginia, and Wyoming.

Special Categories and Complex Scenarios

Insulin and Diabetic Supplies

Insulin receives special treatment reflecting its life-sustaining necessity. Nearly every state exempts prescription insulin from sales tax. Illinois applies its 1% reduced rate rather than full exemption.

Many states extend exemptions beyond prescription insulin to include non-prescription insulin, glucose test strips, lancets, and other diabetic supplies. However, significant exceptions exist. California, Connecticut, Florida, Hawaii, Illinois, Kansas, Kentucky, Louisiana, Massachusetts, New Mexico, North Dakota, Utah, West Virginia, and Wyoming tax some or all diabetic supplies even when prescribed.

For diabetes supply retailers, state-by-state configuration is essential. The same glucometer test strips may be exempt in New York but taxable in California. Without proper setup, you either overtax customers or face audit liability for uncollected tax.

Medical Devices vs. Medicines

State tax codes often distinguish between medical supplies and medicines, treating them differently for tax purposes. While prescribed medications receive exemption, medical supplies may not, even when prescribed for medical use.

Prosthetic devices classified as medicines typically receive exemption when prescribed. However, durable medical equipment like wheelchairs, hospital beds, and breathing machines face inconsistent treatment. Some states exempt durable medical equipment when prescribed for home use. Others tax it regardless of medical necessity.

Medicare and Medicaid billing affects taxability in certain states. Products and services that can be billed to Medicare/Medicaid may receive automatic exemption in some jurisdictions, based on the theory that government healthcare programs shouldn’t incur state sales tax.

For businesses selling both medications and medical supplies, this creates classification challenges. Proper product categorization in your tax system becomes critical to accurate collection.

Cosmetic Procedures and Drugs

Drugs used in cosmetic procedures may be taxable even in states that exempt prescription medicines. The key distinction is therapeutic use versus cosmetic use.

Botulinum toxin prescribed for medical conditions like migraines or excessive sweating typically qualifies for exemption as a prescribed medicine. The identical drug used for cosmetic wrinkle reduction may be taxable as part of a cosmetic service.

Dermal fillers, chemical peels, and similar products face similar scrutiny. Even with a doctor’s involvement, if the purpose is cosmetic enhancement rather than treatment of a medical condition, the drugs involved may not qualify for standard prescription drug exemptions.

For medical spas and cosmetic practitioners, this creates compliance complexity. The same inventory may be exempt or taxable depending on documented use. Many states require separate tracking and documentation for cosmetic versus therapeutic uses.

Animal Medications

Veterinary medications receive less favorable tax treatment than human pharmaceuticals in most states. While the same chemical compounds may be involved, animal health products face different rules.

Most states treat animal medications differently from human medications. Prescription status alone doesn’t guarantee exemption for veterinary drugs. Some states require veterinary prescriptions to be written on specific forms or by licensed veterinarians meeting state-specific criteria.

Generally, animal medications are taxable unless specifically exempted by state law. States with broad medical exemptions may include veterinary prescriptions, but many do not. For businesses selling both human and animal medications, separate compliance strategies are necessary.

Farm animal medications sometimes receive agricultural exemptions distinct from medical exemptions. These agricultural exemptions may be broader or narrower than prescription drug exemptions, depending on the state’s agricultural policy priorities.

Navigating Gray Areas: When Definitions Matter

What Counts as a “Medicine”?

Federal definitions provide a baseline through FDA recognition and inclusion in official pharmacopeias. However, states exercise considerable latitude in adopting or modifying these definitions.

The United States Pharmacopeia, Homeopathic Pharmacopeia, and National Formulary represent federal standards for drug recognition. Substances listed in these references generally qualify as medicines under state law. However, state definitions can include additional substances or exclude certain categories.

Supplements, vitamins, and herbal preparations occupy a gray area. Some states exempt these products when prescribed by licensed healthcare providers. Others tax them regardless of prescription status, classifying them as supplements rather than medicines.

State-specific definitions can include or exclude entire product categories. One state may exempt compounded medications prepared by pharmacists. Another may require FDA approval for exemption, thereby taxing compounded preparations. These variations demand state-specific research for accurate compliance.

Prescribed vs. Over-the-Counter

The distinction between prescribed and OTC medications creates compliance challenges beyond simple product classification. The transformation of an OTC product into a prescribed product affects taxability in most states.

When a healthcare provider writes a prescription for an OTC medication, most states treat that transaction as exempt. The prescription converts the taxable OTC product into an exempt prescribed medication. This principle applies broadly. A customer purchasing omeprazole OTC pays tax, while a customer with a prescription for the identical product receives it tax-free.

However, prescription requirements for exemption vary by state and product type. Some states require prescriptions to meet specific formatting requirements. Others accept any written authorization from a licensed healthcare provider. A few states explicitly exclude certain OTC products from exemption even when prescribed.

Documentation requirements create operational challenges. Pharmacists must maintain records proving prescription status at the time of sale. For audit purposes, you must be able to demonstrate that exempt sales were indeed prescribed. This means preserving prescription records, maintaining point-of-sale documentation linking sales to prescriptions, and ensuring your systems track exempt transactions.

Compliance Challenges for Multi-State Sellers

Key Challenges

Multi-state prescription drug sales create compliance complexity that increases exponentially with geographic expansion.

Inconsistent Definitions: What qualifies as a prescription drug in one state may not meet another state’s criteria. Medical marijuana prescriptions, compounded medications, and combination products face particularly inconsistent treatment. Your systems must account for state-specific definitions rather than applying universal rules.

Changing Regulations and Nexus Requirements: States regularly update tax laws, nexus thresholds, and compliance requirements. Economic nexus rules mean crossing $100,000 in sales or 200 transactions can trigger new collection obligations. For businesses growing quickly, monitoring where you’ve established nexus is essential to avoiding penalties for failing to collect tax where required.

Documentation and Record-Keeping Obligations: Proving prescription status during audits requires comprehensive documentation. You must maintain records showing prescription authorization, pharmacy dispensing, and the exempt nature of each transaction. These records must be preserved for the statute of limitations period, typically 3-5 years depending on the state.

Risk of Overpaying or Underpaying Sales Tax: Configuration errors in sales tax automation platforms create dual risks. Overtaxing prescriptions damages customer relationships and creates refund obligations. Undertaxing non-exempt items leaves you liable for uncollected tax plus penalties and interest during audits.

Automation Platform Configuration Errors: Sales tax software requires careful setup to handle prescription drugs correctly. Common mistakes include treating all pharmacy sales as exempt (missing OTC products that should be taxed), applying wrong rates (like full tax instead of Illinois’s 1% rate), and misclassifying products based on inadequate data.

Common Mistakes

Failing to Update State-Specific Rules: State tax laws change regularly. A state that taxed a product category may enact an exemption. Economic nexus thresholds adjust. Without regular updates to your tax software and configuration, you operate on outdated rules that create liability.

Misclassifying OTC Products: In states that exempt OTC medications, businesses sometimes fail to update systems and continue collecting tax. This overtaxation creates customer complaints and refund obligations. Conversely, in states that tax OTC drugs, classifying them as exempt creates audit exposure.

Not Maintaining Proper Prescription Documentation: During audits, you must prove exempt sales were legitimately exempt. Without prescription records linking to sales transactions, you may owe tax on previously exempt sales plus penalties. This is particularly problematic for online pharmacies where documentation practices may be less robust than traditional pharmacies.

Overlooking Local Tax Implications: State-level exemptions don’t always extend to local jurisdictions. Louisiana’s parish taxes on prescriptions exemplify this. Illinois exempts local taxes on prescriptions despite charging state tax. Without address-level validation, you may under-collect or over-collect local taxes.

How to Ensure Accurate Sales Tax Compliance

Best Practices

Conduct a Nexus Analysis: Identify all states where you’re required to collect sales tax. Economic nexus means remote sellers must monitor sales volume by state. HOST’s nexus analysis service examines your sales data to determine precisely where you’ve triggered collection obligations.

Research Each State’s Specific Definitions: Don’t assume universal rules apply. Research how each state defines prescription drugs, what documentation is required, and which healthcare providers can write qualifying prescriptions. This state-specific research forms the foundation of compliant configuration.

Implement Proper Documentation Systems: Verify prescription status for exempt sales and maintain records linking prescriptions to transactions. For online sales, integrate prescription verification into your checkout process. For retail locations, ensure point-of-sale systems capture prescription information.

Configure Sales Tax Software Correctly: Set up your automation platform with accurate product classifications. Create separate categories for prescription drugs, OTC drugs in exempt states, OTC drugs in taxable states, and special cases like insulin. Apply the correct tax rate for each category in each state, including Illinois’s 1% rate and Louisiana’s parish-level rules. HOST offers a free sales tax software review to identify and fix configuration errors before they become costly.

Maintain Detailed Records: Preserve documentation of all medication sales and exemption claims. During audits, you must produce records demonstrating the exempt nature of untaxed sales. Industry best practice is retaining records for at least five years.

Review Compliance Quarterly: Regulations change continuously. Conduct quarterly reviews of your state-by-state obligations, nexus status, and software configuration. This proactive approach catches issues before they become audit problems.

When to Seek Expert Help

Certain situations demand professional expertise to avoid costly mistakes:

- Selling prescription or non-prescription medications across multiple states: The complexity of state-by-state rules makes professional guidance valuable.

- Dealing with ambiguous product classifications: Products that straddle categories (supplement vs. drug, cosmetic vs. therapeutic) benefit from expert analysis.

- Considering expansion into new markets: Before entering new states, understanding the full compliance picture prevents surprises.

- Facing audit or compliance issues: Professional representation during audits can minimize liability and protect your interests.

HOST specializes in sales tax compliance for businesses selling across state lines. Our services include nexus analysis, registration, filing, notice management, audit defense, and voluntary disclosure agreements. With over 25 years focused exclusively on sales tax, we handle the complexity so you can focus on growth.

Next Steps: Get Compliant Without the Headache

Sales tax compliance for prescription drugs doesn’t have to consume your time or create constant worry. Understanding the fundamentals: prescription drugs are exempt in 44 states, Illinois charges 1%, and special circumstances exist, provides a foundation. But translating that knowledge into accurate multi-state compliance requires expertise and systems.

Whether you’re unsure about classification, concerned about configuration errors, or simply want to offload the burden entirely, Hands Off Sales Tax is ready to help. We’ve been 100% focused on sales tax since 1999, helping businesses navigate compliance so you can keep your hands on your business.

Contact HOST today to discuss your needs or schedule a free consultation. Our team has assisted businesses just like yours for decades, so you can trust us to get it right.

Want to learn more? Get our “10 Sales Tax Mistakes E-Commerce Sellers Make” e-book to identify and avoid common pitfalls.

Frequently Asked Questions

Are prescription drugs taxed in all states?

No. Prescription drugs are exempt from sales tax in 44 of 45 states with sales tax. Illinois is the only exception, taxing prescriptions at a reduced 1% rate compared to its 6.25% standard rate. The five states without sales tax (Alaska, Delaware, Montana, New Hampshire, and Oregon) don’t tax any retail sales, including prescriptions.

Can I get an exemption for over-the-counter medicines?

It depends on your state. Nine states plus Washington D.C. exempt OTC medications universally: Connecticut, Florida, Maryland, Minnesota, New Jersey, New York, Pennsylvania, Texas, Vermont, and Virginia. In most other states, obtaining a doctor’s prescription typically qualifies the OTC product for exemption, with Georgia being a notable exception that taxes OTC drugs even when prescribed.

What about insulin and diabetes supplies?

Insulin is exempt on prescription in all states except Illinois, which applies a 1% rate. Many states also exempt non-prescription insulin, glucose test strips, and test lancets. However, significant exceptions exist in California, Connecticut, Florida, Hawaii, Illinois, Kansas, Kentucky, Louisiana, Massachusetts, New Mexico, North Dakota, Utah, West Virginia, and Wyoming, where some or all diabetic supplies may be taxable.

Does my pharmacy location affect which tax rules apply?

Yes. If you have sales tax nexus in multiple states, you must follow each state’s individual rules. Physical location, warehouse presence, or sufficient sales volume (economic nexus) can trigger requirements in new states. For online pharmacies, customer location determines applicable tax—not your business location.

Why does my sales tax software calculate different amounts by state for the same medication?

Each state has unique definitions, exemptions, and rates. The same prescription drug might be fully exempt in most states, charged at 1% in Illinois, and subject to local taxes in certain Louisiana parishes. Accurate configuration requires state-specific knowledge. Misconfiguration is common and costly, which is why professional review is recommended.

What documentation do I need to maintain for prescription drug exemptions?

Keep copies of prescriptions, records indicating prescription status at time of sale, and pharmacy records showing authorization to dispense. These documents substantiate exemption claims if audited. Industry best practice is retaining records for at least five years, though some states have longer statute of limitations periods.

Are prescription drugs sold to hospitals taxable?

Usually no, but rules vary. Most states exempt prescription drugs regardless of purchaser. However, South Carolina and Hawaii limit exemptions to direct patient sales, potentially taxing sales to hospitals and medical facilities. For pharmaceutical distributors, understanding customer-type rules is essential.

How do I handle prescription drugs sold across state lines in my e-commerce business?

You must comply with the laws of the state where the customer receives the medication. Conduct a nexus analysis to determine your obligations, then configure each state’s rules correctly in your system. This includes understanding which states you’re required to collect tax in and properly classifying products for each jurisdiction.

Can I get a refund if I’ve been incorrectly collecting sales tax on prescriptions?

Possibly. Consider filing a voluntary disclosure agreement (VDA) with affected states to limit lookback periods and reduce penalties. However, refunding customers you overtaxed creates operational challenges. Professional guidance is essential to maximize recovery while minimizing complications. HOST’s VDA services can help navigate this process.

What’s the difference between Georgia and other states’ OTC rules?

Georgia exempts prescription medications but taxes OTC products, even if purchased under prescription. This is unusual. In most states, obtaining a prescription for an OTC product renders it exempt. Georgia maintains the taxable status regardless of prescription, requiring special attention for retailers serving Georgia customers.