Crossing $100,000 in Nebraska sales triggers collection obligations most e-commerce sellers don’t see coming. Nebraska sales tax nexus determines whether your business must register, collect, and remit sales tax regardless of physical presence.

Miss the threshold, and you’re facing back taxes, penalties, and audit risk. Navigate it correctly, and Nebraska becomes just another manageable jurisdiction in your compliance portfolio.

Hands Off Sales Tax (HOST) specializes in exactly this challenge: determining where you have nexus, handling registrations, and managing ongoing filings so Nebraska’s requirements never become a distraction.

What Is Sales Tax Nexus?

Sales tax nexus is the connection between your business and a state that creates a tax collection obligation. Once you establish nexus in Nebraska, you must register for a sales tax permit, collect the appropriate tax from customers, and file returns with the Nebraska Department of Revenue.

Nexus comes in two forms: physical nexus (traditional presence like stores or warehouses) and economic nexus (reaching sales thresholds without physical presence). The 2018 South Dakota v. Wayfair Supreme Court decision gave states authority to require remote sellers to collect sales tax based purely on economic activity.

Nebraska adopted economic nexus immediately after Wayfair, joining 45+ states now requiring remote sellers to track sales and comply once thresholds are crossed.

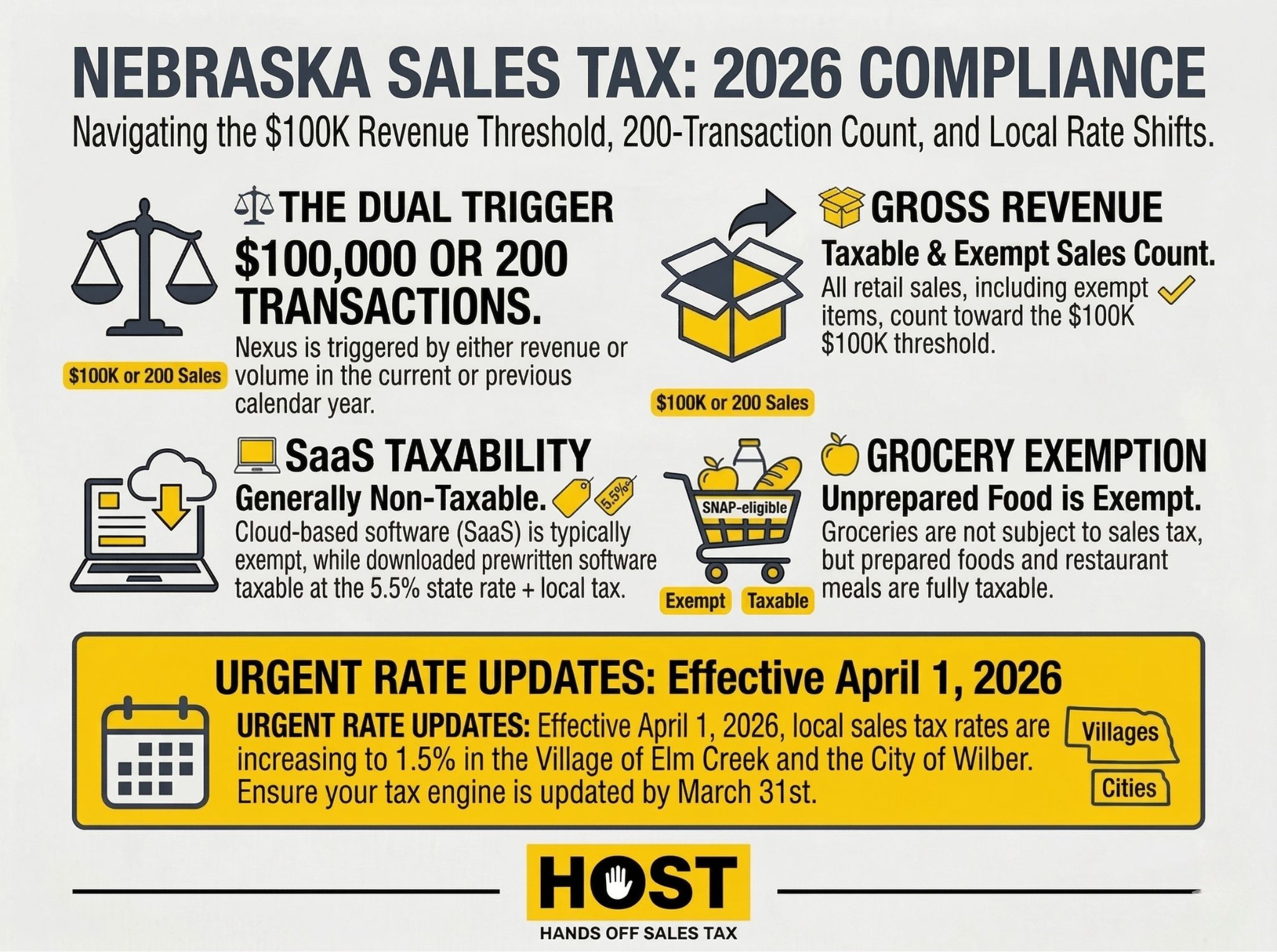

Economic Nexus: The $100,000 Threshold

Nebraska’s economic nexus law triggers when your business exceeds $100,000 in gross revenue from sales into Nebraska during the current or previous calendar year. There’s no transaction count threshold. Only the revenue number matters.

This $100,000 includes all retail sales delivered to Nebraska customers, whether taxable or exempt. Sold $105,000 worth of products to Nebraska buyers in 2024, even if $20,000 were exempt items? You’ve met the threshold.

Key details:

- Measurement Period: Current or previous calendar year. Cross $100,000 in 2025? You have nexus. Crossed it in 2024? You still have nexus in 2025.

- Gross Revenue: Total sales, not just taxable sales. Exempt items count toward the threshold.

- No Grace Period: Registration is required once you meet the threshold. Nebraska expects compliance immediately.

For e-commerce businesses experiencing growth, this threshold arrives faster than expected. A successful Q4 can push you over $100,000, triggering obligations for the following year even if sales normalize.

HOST’s nexus analysis identifies precisely when you’ve crossed Nebraska’s threshold and every other state’s, so you’re never caught off guard.

Physical Nexus: Traditional Triggers

Physical nexus creates obligations regardless of sales volume. Even $1 in sales combined with physical presence requires registration.

Physical nexus in Nebraska includes:

- Retail Locations: Stores, kiosks, or pop-up shops

- Warehouses and Fulfillment Centers: Inventory stored in Nebraska, including third-party logistics (3PL) arrangements

- Employees: Sales staff, remote workers, or representatives operating in Nebraska

- Affiliate Relationships: In-state businesses or affiliates who design products you sell, solicit sales on your behalf, or provide fulfillment services

- Temporary Presence: Trade shows, conventions, or craft fairs where sales occur

- Property: Owned or leased property, vehicles, or equipment

The critical consideration for e-commerce sellers: Amazon FBA and third-party warehouses create physical nexus. If Amazon stores your inventory in a Nebraska fulfillment center, even temporarily, you have physical nexus. You may not control where Amazon places your products, but Nebraska still expects compliance.

Marketplace Facilitator Laws: When Amazon Collects for You

Nebraska’s marketplace facilitator law requires platforms like Amazon, eBay, Etsy, and Walmart to collect and remit sales tax on behalf of third-party sellers. This law took effect April 1, 2019.

When a marketplace facilitator collects tax on your sales, you generally don’t need to collect again on those specific transactions. However, this doesn’t eliminate your nexus, it just shifts collection responsibility for marketplace sales.

Critical considerations:

- Direct Sales Still Require Collection: Sales through your own website, Shopify store, or other non-marketplace channels require you to collect tax if you have nexus

- Nexus Still Exists: Even if Amazon collects for marketplace sales, you still have nexus from the presence or activity that triggered it

Many e-commerce businesses operate hybrid models, selling both on marketplaces and direct channels. You need to track which sales the marketplace handles and which require your own collection.

HOST manages this complexity, ensuring you’re collecting correctly on direct sales while avoiding double-taxation.

Nebraska Sales Tax Rates: State and Local Considerations

Nebraska’s state sales tax rate is 5.5%. Local jurisdictions add their own rates, making the combined rate higher in many areas.

Combined rates in Nebraska range from 5.5% to 7.5%. Major cities include:

- Omaha: 7.0% (5.5% state + 1.5% local)

- Lincoln: 7.25% (5.5% state + 1.75% local)

- Bellevue: 7.0% (5.5% state + 1.5% local)

- Grand Island: 7.0% (5.5% state + 1.5% local)

The complexity: rates are destination-based, meaning you charge tax based on where the customer receives the product, not where your business is located. Shipping to different Nebraska ZIP codes means different tax rates on identical products.

With 500+ local jurisdictions potentially involved, manual rate management creates significant error risk. Most e-commerce businesses use sales tax automation software, but misconfiguration leads to overcharging customers or undercharging states.

HOST offers a Free Sales Tax Software Review to audit your tax calculation setup, identifying errors before they impact your bottom line.

What’s Taxable in Nebraska?

Most tangible personal property is taxable in Nebraska. Key exceptions include groceries (unprepared food), prescription drugs, and medical devices. Prepared food and restaurant meals are taxable.

For tech businesses: Software-as-a-Service (SaaS) is generally non-taxable in Nebraska, though downloaded software may be taxable depending on how it’s delivered. This distinction matters for cloud-based businesses.

Registration and Filing Requirements

Once you’ve established nexus in Nebraska, registration is straightforward but detailed. You’ll need to obtain a Nebraska Tax ID through the Department of Revenue’s online system, provide business information (Federal EIN, business structure, NAICS code), and estimate sales volume.

Registration timeline: You must register by the first day of the second calendar month after exceeding the threshold. For example, if you cross $100,000 in March, you must register by May 1st and begin collecting tax immediately.

Registration typically takes 1-2 weeks. Nebraska doesn’t charge a registration fee.

Streamlined Sales Tax benefit: Nebraska is a full member of the Streamlined Sales Tax (SST) program. Businesses can register through the SST system and may qualify for free sales tax calculation and reporting services through Certified Service Providers, which is a significant advantage for small e-commerce sellers managing multi-state compliance.

Filing Frequency depends on your sales volume: monthly, quarterly, or annual. Nebraska assigns your filing frequency based on reported sales. As your business grows, frequency may increase.

The registration process appears simple, but errors create delays. Incorrect NAICS codes, misreported business structures, or incomplete information trigger rejections requiring resubmission.

HOST handles sales tax registration in Nebraska and every other required state, managing the paperwork, follow-up, and state communications.

What Happens If You Don’t Comply?

Nebraska pursues uncollected sales tax aggressively. Consequences include:

- Back Taxes: Nebraska can assess uncollected sales tax for up to four years (longer if fraud is suspected)

- Penalties: 10% penalty on unpaid tax, increasing to 25% for repeated failures

- Interest: Accrues on unpaid tax from the original due date

- Audits: Non-compliant businesses face higher audit risk

The financial impact compounds quickly. A business with $200,000 in annual Nebraska sales collecting an average 7% combined rate owes $14,000 annually. Miss two years, and you’re facing $28,000 in back taxes plus penalties and interest, potentially $35,000+ total.

Beyond money, compliance issues consume time. Responding to Nebraska notices, organizing documentation, and managing audit requests diverts focus from revenue-generating activities.

Voluntary Disclosure Agreements: Limiting Past Liability

If you discover you should have been collecting Nebraska sales tax but weren’t, a Voluntary Disclosure Agreement (VDA) can limit damage.

VDAs allow businesses to come forward voluntarily, typically receiving:

- Limited Lookback Period: Usually 3-4 years instead of unlimited

- Penalty Abatement: Reduced or eliminated penalties (though tax and interest still apply)

- Confidentiality: The process remains confidential

- Amnesty from Prosecution: Protection from criminal charges for past non-compliance

The key: you must come forward before the state contacts you. Once Nebraska initiates an audit or sends a notice, VDA benefits disappear.

HOST manages VDA filings, negotiating with Nebraska on your behalf to minimize lookback periods and secure penalty abatement.

HOST: Your Partner for Nebraska Sales Tax Compliance

Managing Nebraska sales tax nexus, alongside 44+ other states with their own thresholds, rates and rules creates complexity that scales with your business growth.

What HOST Delivers:

- Nexus Analysis: We analyze your sales data to determine exactly when you crossed Nebraska’s threshold

- Sales Tax Registration: We handle the Nebraska registration process, completing paperwork and managing state communications

- Ongoing Filing: We prepare and file your Nebraska returns monthly, quarterly, or annually based on assigned frequency

- Rate Management: We ensure correct rates apply to every Nebraska sale across 500+ local jurisdictions

- Notice Response: We interpret and respond to Nebraska Department of Revenue notices

- Audit Defense: We represent you during audits, organizing documentation and defending your position

- VDA Support: We file voluntary disclosure agreements to limit liability

We’ve been 100% focused on sales tax since 1999. Over 25 years helping businesses navigate multi-state compliance. Founded by Mike Espenshade, with parent company TaxMatrix serving North America’s largest companies, we bring enterprise expertise to e-commerce sellers of all sizes.

You handle the sales, we handle the tax.

Ready to Get Nebraska Compliant?

Nebraska sales tax nexus creates real obligations with real consequences. Whether you’ve just crossed the $100,000 threshold, discovered FBA inventory created physical nexus, or realized you should have been collecting for years, the right response is taking action now.

Every day of non-compliance increases liability. Every notice ignored escalates risk. Every audit unprepared costs more.

At HOST, we eliminate the complexity and stress of sales tax compliance. From determining your Nebraska nexus status to managing ongoing filings across all states, we handle everything so you can focus on growing your business.

Contact HOST today to discuss your Nebraska sales tax situation or schedule a free consultation.

Want to learn more? Get our “10 Sales Tax Mistakes E-Commerce Sellers Make” e-book and discover the costly errors we help businesses avoid every day.

Frequently Asked Questions

What is the economic nexus threshold for Nebraska?

Nebraska’s economic nexus threshold is $100,000 in gross revenue from sales into the state during the current or previous calendar year. There’s no transaction count requirement. Only the revenue threshold matters.

Do I have nexus if Amazon FBA stores my inventory in Nebraska?

Yes. Inventory stored in Nebraska creates physical nexus, even if you don’t control where Amazon places your products. This triggers collection obligations regardless of your sales volume.

Does marketplace facilitator collection eliminate my Nebraska obligations?

Not entirely. While Amazon and other marketplaces collect tax on sales through their platforms, you still must collect on direct sales through your own website or other channels if you have nexus.

What happens if I cross the $100,000 threshold mid-year?

You establish nexus immediately upon crossing the threshold. Nebraska expects registration and collection to begin at that point. Monitor your sales monthly to identify when you’ve crossed into nexus territory.

How far back can Nebraska assess unpaid sales tax?

Generally four years, but longer if fraud or intentional non-compliance is suspected. Voluntary disclosure agreements can limit the lookback period to 3-4 years while reducing penalties.

Is SaaS taxable in Nebraska?

Software-as-a-Service (SaaS) is generally non-taxable in Nebraska when customers only access software hosted on your servers. However, downloaded or transferred software may be taxable. If you sell SaaS or digital products, consult with a tax professional to determine your specific obligations.