Understanding Idaho sales tax nexus determines whether your business must collect and remit sales tax in the state. For e-commerce sellers, nexus rules directly impact compliance obligations, pricing strategies, and potential audit exposure.

Idaho’s economic nexus threshold sits at $100,000 in annual sales. Cross it, and collection requirements begin immediately. Between physical presence rules, marketplace facilitator laws, and ongoing filing obligations, navigating Idaho requires clarity on what triggers collection, when to register, and how to stay compliant.

That’s where Hands Off Sales Tax (HOST) delivers. With over 25 years specializing exclusively in sales tax compliance, we analyze your Idaho nexus status, handle registration complexities, and manage ongoing filings so you can focus on scaling revenue.

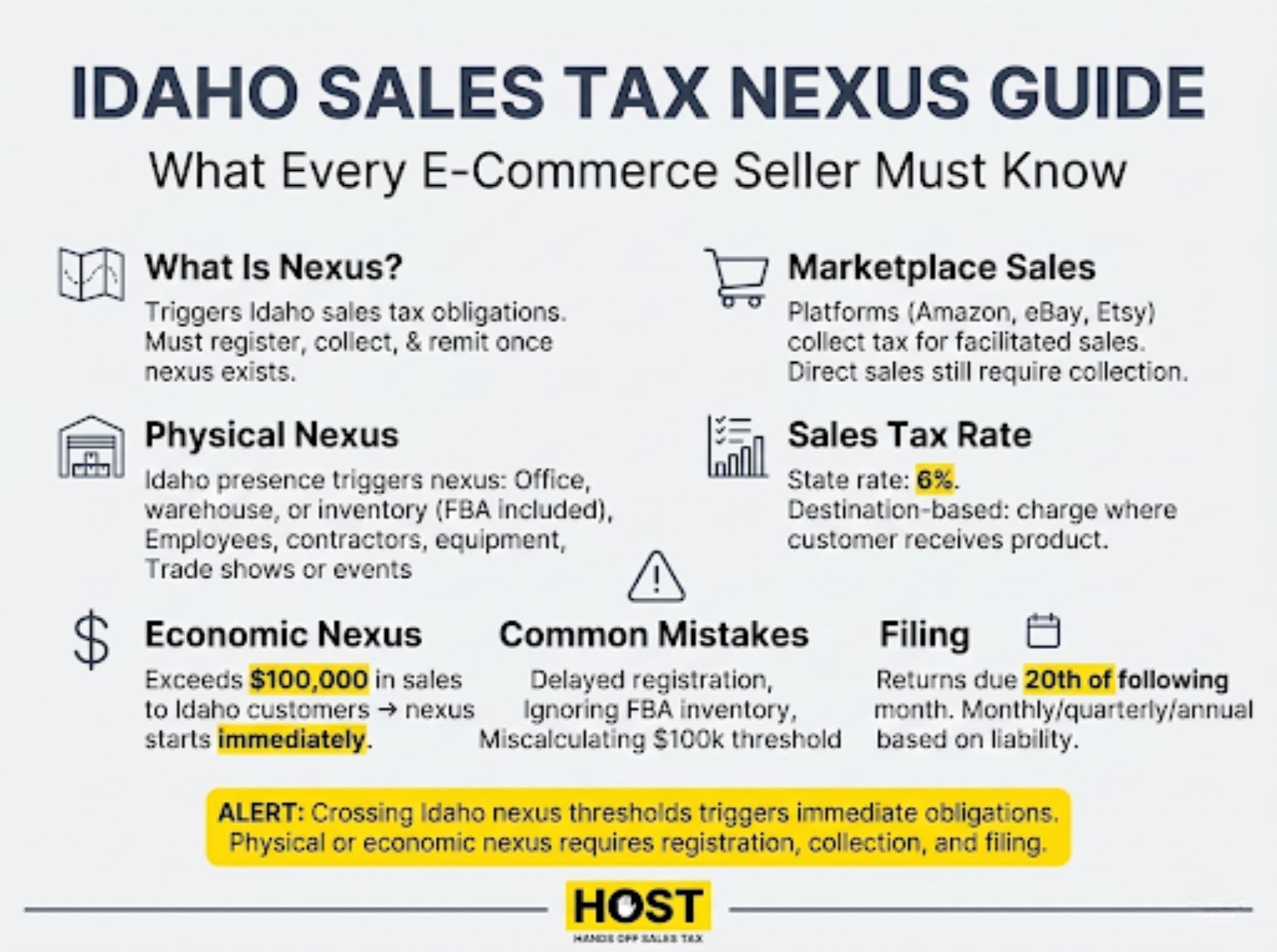

What Is Sales Tax Nexus?

Sales tax nexus is the connection between your business and a state that creates an obligation to collect and remit sales tax. Without nexus, you have no collection responsibility. Once nexus exists, you must register, collect appropriate tax, file returns, and remit payments to the Idaho State Tax Commission.

The concept originated when states could only tax businesses with physical presence like stores, warehouses, employees. The 2018 Wayfair decision changed everything, allowing states to establish economic nexus based solely on sales volume.

Idaho adopted economic nexus immediately following Wayfair. Remote sellers without any physical presence can trigger nexus simply by exceeding sales thresholds. This fundamentally changed compliance for online retailers, marketplace sellers, and any business shipping to Idaho customers.

Idaho Economic Nexus: The $100,000 Threshold

Idaho sales tax nexus triggers when your business exceeds $100,000 in gross sales to Idaho customers in the current or previous calendar year. This includes all sales: taxable and exempt, wholesale and retail.

Cross $100,000, and nexus exists immediately. Idaho requires registration and collection “as soon as practicable,” generally interpreted as within 30 days. There’s no grace period. Hit $100,000 on September 15th, you have nexus starting that day.

Key threshold details:

- Measurement Period: Current or previous calendar year (January 1 – December 31)

- Amount: $100,000 in gross sales shipped to Idaho addresses

- Transaction Count: None—Idaho only uses the dollar threshold

- Calculation: Includes all sales. Exempt items, wholesale transactions, and marketplace sales count toward the threshold

When the Clock Starts

If you exceeded $100,000 in Idaho sales during 2024, you have nexus throughout 2025 even if current-year sales are minimal. The lookback period means nexus can exist based on prior performance.

For new businesses, nexus begins when you first cross $100,000 in the current calendar year. Monitor Idaho sales closely as you approach the threshold, so waiting creates months of uncollected tax liability.

Physical Presence Nexus in Idaho

Economic nexus isn’t the only trigger. Physical presence creates nexus regardless of sales volume. Even $1 in sales combined with physical presence requires collection.

Physical nexus exists when you maintain:

- Retail locations or offices: Any store, showroom, or office space

- Warehouse or inventory: Including fulfillment centers, 3PL facilities, or Amazon FBA inventory stored in Idaho

- Employees or contractors: Sales reps, remote workers, or contractors performing services

- Property or equipment: Owned or leased equipment, vehicles, or tangible property

- Temporary presence: Trade shows, conferences, or pop-up events

Many e-commerce sellers unknowingly trigger physical nexus through FBA. When Amazon stores your inventory in an Idaho fulfillment center, you have physical presence. Amazon’s marketplace facilitator collection doesn’t eliminate your nexus, it just handles the collection obligation for those specific sales.

Other Nexus Triggers: Affiliate and Click-Through

Idaho maintains two additional nexus types that can catch businesses off-guard:

Affiliate Nexus applies when you have related business entities in Idaho. If an Idaho-based company shares ownership, uses substantially similar branding, or provides services that benefit your out-of-state business, you have affiliate nexus once Idaho sales exceed $100,000. This targets parent-subsidiary relationships and shared brands operating across state lines.

Click-Through Nexus triggers when Idaho-based affiliates or referral partners earn commissions directing customers to your business through links or referrals. Once commissions paid to Idaho referrers exceed $10,000 in a 12-month period, you’ve established nexus. This applies to affiliate marketing programs, influencer partnerships, and referral arrangements.

Marketplace Facilitator Laws: When Amazon Collects for You

Idaho’s marketplace facilitator law requires platforms like Amazon, eBay, Etsy, and Walmart to collect and remit sales tax on behalf of third-party sellers. This law took effect October 1, 2019.

When a marketplace facilitator handles a transaction, they’re responsible for collecting Idaho sales tax and filing returns. The seller is relieved of collection responsibility for those specific transactions.

However, marketplace facilitator laws don’t eliminate your nexus. You still have nexus if you meet thresholds, you just don’t collect on marketplace-facilitated sales.

- Marketplace sales only: If 100% of Idaho sales occur through facilitating marketplaces, you typically don’t need to register

- Mixed channel sales: If you sell through your website, non-facilitating platforms, or wholesale channels, you need to register and collect tax on non-marketplace sales

- Nexus monitoring: Even if marketplaces collect everything today, monitor your nexus status for potential changes

Registering for an Idaho Seller’s Permit

Once you establish nexus, registration with the Idaho State Tax Commission is required before collecting sales tax.

Idaho offers online registration through the Taxpayer Access Point (TAP) system at tax.idaho.gov. Processing typically takes 7-10 business days. Idaho issues a seller’s permit number you must include on invoices and when filing returns.

Important details:

- No fee: Idaho charges nothing for a seller’s permit

- Timeline: Register within 30 days of establishing nexus

- Renewals: No renewal required. Permits remain active until you close your business

- Small seller exemption: Starting July 1, 2025, Idaho resident businesses with gross receipts under $5,000 annually are exempt from collection requirements. This exemption does NOT apply to out-of-state sellers.

Idaho Sales Tax Collection Requirements

After registration, collect Idaho sales tax on all taxable sales to Idaho customers.

State and Local Rates

Idaho has a 6% state sales tax rate with limited local additions. Unlike many states with complex varying rates, Idaho maintains uniform statewide taxation for most transactions, simplifying calculation significantly. A few resort cities (like Sun Valley and Ketchum) can impose additional local option tax up to 3%, but remote sellers only collect the 6% state rate.

What’s Taxable in Idaho

Idaho taxes most tangible personal property including physical products, digital products (downloaded software, e-books, music, streaming services), and certain services related to tangible property.

Common exemptions include groceries (unprepared food), prescription medications, manufacturing and agricultural equipment, and certain medical devices.

Shipping and Handling

Idaho taxes shipping charges differently based on how you bill them. If you separately state shipping on the invoice, it’s not taxable. If you include shipping in the product price, the entire amount becomes taxable. Best practice: always separate shipping charges on invoices to avoid overtaxing customers.

Idaho Sales Tax Filing and Remittance

Idaho requires periodic filing of sales tax returns and remittance of collected tax. Filing frequency depends on your tax liability:

- Monthly: Businesses collecting $500+ per month file monthly by the 20th of the following month

- Quarterly: Businesses collecting less than $500 monthly file quarterly

- Annually: Very small sellers (under $200 per month) may file annually with permission

Most e-commerce sellers exceeding the $100,000 nexus threshold file monthly.

Idaho requires electronic filing through the TAP system. Returns include gross sales, exempt sales, taxable sales, tax collected, and any deductions or credits. Payment must accompany returns. Even if you made zero sales during a period, you must file a zero return. Failure to file triggers penalties even when no tax is due.

Late Filing Penalties

Idaho assesses penalties for late filing and late payment:

- Late filing: 5% of tax due per month (maximum 25%)

- Late payment: 1% per month plus interest

These penalties compound quickly. A return two months late incurs 10% late filing penalty plus 2% late payment penalty. Substantial on any meaningful tax liability.

HOST manages all Idaho filing deadlines, ensuring returns are filed accurately and on time across all states where you have nexus, preventing costly penalties while freeing your time for revenue-generating activities.

Common Idaho Nexus Pitfalls

“I Only Sold Through Amazon—Do I Need to Register?”

If 100% of Idaho sales occurred through marketplace facilitators, you typically don’t need to register. However, if you also sell directly through your website, wholesale channels, or non-facilitating platforms, you must register and collect on those sales.

“I Hit $100,000 Last Year But Not This Year—Do I Still Have Nexus?”

Yes. Idaho’s lookback provision means if you exceeded $100,000 in the previous calendar year, you maintain nexus throughout the current year regardless of current sales levels.

“What If I Discover I Should Have Been Collecting?”

If you determine you’ve had nexus but haven’t been collecting, address it immediately through a Voluntary Disclosure Agreement (VDA). Idaho’s VDA program allows you to come forward, limit lookback periods (typically 3 years instead of unlimited), and potentially abate penalties.

HOST manages VDAs with states, negotiating favorable terms that limit your liability while bringing you into compliance, which is critical when discovering past nexus.

Why Idaho Nexus Compliance Matters

Non-compliance creates significant risks:

Financial Liability: Idaho can assess back taxes for every sale where you should have collected but didn’t. On $500,000 in uncollected Idaho sales over three years, you’d owe $30,000 in back taxes plus penalties and interest, potentially $40,000+ total.

Audit Risk: Idaho cross-references marketplace facilitator data, sales tax software providers, and payment processors to identify non-compliant sellers. Once flagged, audits examine multiple years of transactions.

Growth Limitations: Unresolved nexus creates liability that can derail financing, acquisition, or exit opportunities. Due diligence uncovers non-compliance, tanking valuations or killing deals entirely.

Proactive compliance costs far less than reactive remediation.

HOST: Your Partner for Idaho Nexus Compliance

Managing Idaho nexus is straightforward compared to states with complex local rates, but it’s still one piece of a 45-state puzzle. HOST ensures you’re compliant everywhere you have nexus while minimizing operational burden.

What HOST Delivers

Nexus Analysis: We analyze your sales data and physical footprint to determine exactly where you’ve met Idaho and other state thresholds, eliminating guesswork.

Idaho Registration: We handle Idaho seller’s permit applications, completing paperwork and following up with the Tax Commission.

Sales Tax Filing: HOST files your Idaho returns monthly, quarterly, or annually, ensuring accuracy and on-time remittance.

Multi-State Management: We manage nexus and filing obligations across all 45+ sales tax states.

Notice Response: We handle Idaho Tax Commission notices or inquiries, interpreting requirements and responding appropriately.

Audit Defense: If Idaho audits your business, we organize documentation, communicate with auditors, and work to minimize liability.

VDA Services: For businesses discovering past nexus, we file voluntary disclosure agreements with Idaho to limit lookback periods and abate penalties.

We’ve focused exclusively on sales tax since 1999. That’s over 25 years helping businesses navigate compliance complexities. Founded by Mike Espenshade, with parent company TaxMatrix serving North America’s largest companies, we bring enterprise expertise to e-commerce sellers of all sizes.

You handle the sales, we handle the tax.

Ready to Address Idaho Nexus?

If you’re selling to Idaho customers, understanding your nexus status is the first step toward proper compliance. Whether you’re crossing the $100,000 threshold for the first time, discovering past obligations, or overwhelmed by managing Idaho alongside dozens of other states, professional guidance eliminates stress and prevents costly mistakes.

HOST combines deep technical expertise with 25+ years of specialized experience, transparent communication, and personalized support. When you’re ready to ensure Idaho compliance supports growth rather than hindering it, we’re ready to help.

Contact HOST today to discuss your Idaho nexus situation or schedule a free consultation. Let us handle the complexity so you can focus on scaling your business.

Want to learn more? Get our “10 Sales Tax Mistakes E-Commerce Sellers Make” e-book.

Frequently Asked Questions

What is the Idaho sales tax nexus threshold?

Idaho sales tax nexus triggers when your business exceeds $100,000 in gross sales to Idaho customers in the current or previous calendar year. Once you cross this threshold, you must register and begin collecting sales tax immediately.

Do I need to register in Idaho if I only sell through Amazon?

If 100% of your Idaho sales occur through marketplace facilitators like Amazon, you typically don’t need to register because the marketplace handles collection. However, if you also sell through your own website or other non-facilitating channels, you must register and collect on those direct sales.

What triggers physical presence nexus in Idaho?

Physical presence nexus exists when you maintain employees, inventory (including FBA storage), property, equipment, or offices in Idaho. Even temporary presence through trade shows or events can create nexus. Physical presence requires collection regardless of sales volume.

When must I register after establishing Idaho nexus?

Idaho requires registration “as soon as practicable” after establishing nexus, generally interpreted as within 30 days of exceeding thresholds. Delays beyond this create penalties and interest on uncollected tax.

What is Idaho’s sales tax rate?

Idaho has a uniform 6% statewide sales tax with no local additions for most retail sales. A few resort cities impose limited local taxes on lodging and specific services, but general e-commerce sales face the flat 6% rate.

What happens if I discover I should have been collecting Idaho sales tax?

If you determine past nexus without collection, address it immediately through a Voluntary Disclosure Agreement (VDA). Idaho’s VDA program limits lookback periods (typically 3 years) and can abate penalties, significantly reducing liability compared to waiting for the state to discover non-compliance.